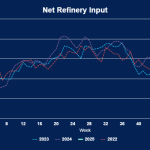

Net refinery input decreased by 250 Mb/d to 16.65 MMb/d, and gross input declined by 275 Mb/d to 18.35 MMb/d last week (see chart below). This marks the beginning of the winter-to-spring maintenance period, which is expected to peak with nearly 2 MMb/d of distillation units going offline by late March, according to IIR Energy. In PADD 3, input dropped by 300 Mb/d due in large part to planned maintenance on January 5th at Marathon’s 631 Mb/d Galveston Bay refinery, which took 290 Mb/d offline, as reported by IIR Energy.

Featured Articles

- Blog

You Crack Me Up - Refiners Increasingly Relying on Hydrocracking Capacity As Fuel Demand Shifts

More than a decade ago, several U.S. refiners brought new hydrocracking capacity online, wagering that rising demand for middle distillates made such major investments necessary. They were good bets. Demand for jet fuel is expected to continue to grow, and while diesel demand is seen as relatively flat in the U.S. over the next few years, it will continue to climb globally through 2045, according to RBN’s recently released Future of Fuels report. In contrast, the report also sees domestic gasoline demand declines accelerating post-2026 and peaking globally by about 2030, as more consumers turn to electric vehicles (EVs). These contrasting trajectories for middle distillates vs. gasoline will put a growing premium on distillate-centric hydrocracking capacity. In today’s RBN blog, we’ll examine trends incentivizing hydrocracking capacity and how these units will allow U.S. refiners to maintain their competitiveness in a rapidly changing product market.

- Blog

(Turn around) Every Now and Then They Need a Little Bit of Maintenance – How Refinery Repairs Impact Exports

Gulf Coast diesel crack spreads (the margin between diesel prices and Light Louisiana Sweet crude - LLS) are averaging just under $16/Bbl this year – about 75 cnts/Bbl lower than 2012 but still pretty healthy. Gulf Coast diesel exports increased by 25 percent in 2012 – mostly to meet increased demand in Latin America. By December Gulf Coast refineries were running at 95 percent capacity to meet export demand. Yet during the first 2 months of 2013 refinery utilization plummeted to 80 percent, diesel production fell and Gulf Coast diesel exports dived by 300 Mb/d. Today we describe the impact that a heavier than usual Gulf Coast refinery repair season had on product exports.