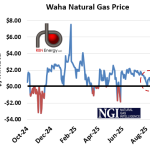

After a modest reprieve in June and July, Permian natural gas prices have moved lower in August, averaging $0.71/MMbtu so far during the month (red dashed oval, chart below) and hitting $0.55/MMbtu on Friday. As usual, constrained natural gas egress capacity is to blame.

Featured Articles

- Blog

Do You Really Want to Hurt Me - Gas Prices at Permian's Waha Hub Roar Higher, Devastating Shorts

What happens when almost everybody is on the same side of a trade and the fundamentals flip? Yup, max pain. Everyone races for the exits at the same time, sending the market into speculative liquidation mode and causing cascading losses. It can get frantic and ugly — tens or even hundreds of millions of dollars are at stake, and no one’s sure how bad things might get. As we discuss in today’s RBN blog, frantic and ugly is precisely what happened over the last few days at the Waha natural gas trading hub in West Texas.

- Blog

Danger Zone - The Outlook for the Appalachian Natural Gas Market

It’s been a while since the Appalachian natural gas market has looked this bullish. Outright cash prices at the Eastern Gas South hub are at multi-year highs. Regional storage inventories are sitting low, setting the stage for supply shortages and still higher prices this winter. But the potential for severe takeaway constraints and basis meltdowns are lurking, and by next year, they could become regular features of the market again like they were in the 2016-17 timeframe, or worse — at least in the spring and fall when Northeast demand is lowest. Regional gas production is still being affected by maintenance and has been somewhat volatile lately as a result, but it averaged 34.5 Bcf/d in June, just 300 MMcf/d shy of the December 2020 record. What’s more, at current forward curve prices, supply output could surpass previous highs by next spring and grow by ~ 5 Bcf/d (15%) by 2023. Outbound flows set their own record highs this spring, running at over 90% of takeaway capacity, and will head higher, which means that spare exit capacity for supply needing to leave the region is shrinking. The handful of planned takeaway expansions that remain are facing environmental pushback and permitting delays, and the few that are targeting completion in the next year may not be enough. Today, we provide the highlights of the latest forecast from our new NATGAS Appalachia report.

- Blog

Let the Sky Fall - From $200/MMBtu to $1/MMBtu Gas, PNW Market Volatility Continues

Three months ago, the Pacific Northwest natural gas market recorded the highest trade in U.S. spot gas price history. The region at the time was dealing with extreme winter heating demand, a pipeline outage that limited access to gas supply and storage deliverability issues –– all of which were compounding constraints in the power markets. The result was a feeding frenzy that led gas prices to skyrocket to as much as $200/MMBtu at the Sumas, WA, hub on March 1. Fast forward to today — prices there have crumbled, falling to as low as $0.80/MMBtu in trading last week. Winter demand has dissipated, pipeline and storage constraints have eased, and the region is now dealing with an entirely different — even opposite — set of problems. Today, we take a closer look at the factors behind these latest price moves.