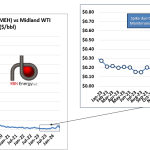

The differential between Permian/Midland WTI crude oil and WTI on the Gulf Coast, represented by Magellan East Houston (MEH), spiked to $1.41/bbl on May 1, and then averaged $0.80/bbl during the month of May (right graph below). That’s the highest monthly average since June 2020. It’s a given that new crude oil pipeline capacity from the Permian to the Gulf Coast will be needed at some point. Was this the signal that indicates that capacity will be needed soon? After all, the differential had averaged a paltry $0.35/bbl during 2021 through 2023, definitely an indication of overcapacity (left graph below).

The wide differential in May was a heads up that capacity is getting tighter. However, the primary culprit that triggered the spike was news of a 10-day early June 2024 maintenance event on the huge 1.5 MMb/d Wink-to-Webster / Enterprise Midland-to-ECHO III combo pipeline. The runup and spike in the differential was primarily due to traders positioning for the outage. By the time the current monthly trade cycle rolled around, market concerns had subsided. The differential so far during June has averaged $0.47/bbl.