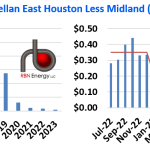

Way back in 2018, Permian crude oil production was soaring, but there was not enough pipeline capacity to handle the volume. The market responded as it always does in such situations, with Permian Midland crude trading at a huge discount to the Gulf Coast (represented by Magellan East Houston, or MEH), with the 2018 spread between Permian and MEH averaging $12/bbl (see left graph below) and peaking at $23.75 in August of that year. But then midstreamers responded and pipelines were built, both to Corpus Christi and to Houston, with pipeline rates for capacity ranging from $1/bbl to $4.75/bbl or more.

In 2019, the market differential declined to $5.50/bbl as surplus capacity came on to the market, but then after the 2020 COVID meltdown and subsequent massive oversupply of capacity, the differential collapsed to $1.25/bbl, then $0.50/bbl in 2021 and a paltry $0.35/bbl in 2022. So far this year, the differential dropped to an average of only $0.21/bbl (right graph). But a few days ago, the differential melted down.