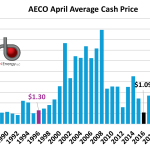

The average cash price of Western Canada’s natural gas benchmark of AECO was C$1.33/GJ ($1.02/MMBtu) in April 2024 (red column in chart below). This is the fourth lowest April average in 28 years with 1996 at $1.30/GJ (purple column), 2016 at $1.09/GJ (black column) and 2019 at $0.94/GJ (green column) being lower. The low price of 1996 was the result of insufficient gas pipeline egress capacity from Western Canada, while 2019 resulted from pipeline constraints that were being imposed on the Alberta pipeline system. The low price of 2016 resulted from the same dynamics that are driving the current weak pricing episode in terms of the market exiting a very warm winter leaving a much greater than average amount of gas in storage and robust supplies in Western Canada.

Featured Articles

Don't Stop, Part 2 - Will Canadian Producers Increase Gas-Focused Spending, Supplies?

Canadian oil and natural gas producers were dancing very much to the same tune as their U.S. counterparts in 2019: reduce capital spending, live within cash flow and improve returns to investors. The only major difference for Canadian gas producers is that they were forced to dance even faster due to abysmal natural gas pricing during the summer of 2019, which cast a very negative pall over the whole sector for the remainder of last year. Although the focus on spending restraint, cash flow and returns has not changed for these producers upon entering 2020, there are encouraging signals that Canadian gas pricing will be materially improved this year, especially during the summer months, supporting higher cash flows and a cautious expansion in capital spending. Today, we examine the drivers behind what might increase capital spending by gas producers and lead to an increase in supplies.

Life Ain't Easy - Canadian Natural Gas Production Facing Another Year of Decline

Canadian gas production in 2019 turned lower for the first time in half a dozen years as very weak benchmark Canadian gas prices led to a sharp reduction in drilling and wellhead shut-ins. This year, higher prices, more drilling, and greater pipeline egress capacity were supposed to set the stage for a return of supply growth. Instead, production volumes have slipped further due to reduced drilling activity and, more recently, a spate of maintenance work. And even if there is some improvement in the next few months, annual average production looks to be on track for a second consecutive decline in 2020. But what about next year? Today, we take a closer look at the recent supply trends and whether there are any signs pointing to a production rebound in 2021.