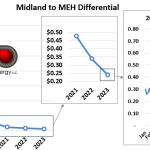

Crude oil takeaway out of the Permian was massively overbuilt to about 3.0 MMb/d in 2021-22 when the combined Wink-to-Webster/Midland-to-Echo projects came online. As shown in the left graph below, the differential between Midland and Houston (Magellan East Houston, or MEH), had been about $12/bbl in 2018 and $5/bbl in 2019, but by 2022, was down to $0.34/bbl (middle graph), then down to average only $0.24/bbl in 2023. But recently the differential has started showing signs of life, spiking up to more than $0.50/bbl in three weekly averages since September 2023, which includes last week (right graph). The implication is that pipelines out of the Permian are starting to fill.

For one thing, the pipelines to Corpus are maxed out, with barrels being pulled to the Enbridge and Gibson terminals at Ingleside that can load the large, VLCCs providing lower shipping costs to exporters. Beyond that export corridor, the prospects for much more crude moving out of the Permian to either Cushing or Nederland look doubtful, so that means the only viable outlet is to Houston. And there is still somewhere in the neighborhood of 450 Mb/d of capacity remaining on that corridor after you subtract Enterprise Seminole being converted back to NGL service and, depending on how you count volumes on a couple of the legacy pipelines going that direction. But Permian crude oil production will be increasing at least 300 Mb/d in 2024. That would not fill the Houston pipes to the brim, but it does imply that only about 150 Mb/d capacity is left before Permian barrels are forced into less attractive – non-Houston - markets. Is that enough to bring the Midland to MEH differential back above $1/bbl? See our annual Prognostications blog on January 2 for the answer.