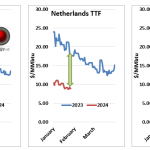

In early 2023, a year after Russia first invaded Ukraine, natural gas markets in Europe and Asia were still in turmoil, as fears of gas shortages continued to loom over Europe, keeping global prices for natural gas and LNG high. Last year at this time (Jan 22-26 weekly average, green arrow pointing to blue line, left graph), the price of LNG in Asia (as measured by the JKM index) was $21.85/MMbtu, while the price in Europe (as measured by Netherlands TTF, middle graph) was $19.30/MMbtu. To put that in perspective back then Henry Hub (right graph) was $3.20/MMbtu.

Featured Articles

- Blog

Anticipation - Did Putin Pop the Global Natgas Bubble, or Give Europe a Last Chance to Stock Up?

For six months, European natural gas prices skyrocketed higher almost every day. The soaring prices made sense. Gas inventories in Europe were low following higher-than-normal demand last winter. Economies were recovering from COVID-19. Russia was curtailing gas deliveries. It all added up to a likely supply shortage during the winter of 2021-22. And the market did what markets do: anticipate. Even though the next winter season was months away, gas buyers went to work, stocking up on supplies like squirrels gathering nuts. The more prices increased, the more panic buying kicked in. By last Tuesday, October 5, the European TTF price was up more than 5X what it had been on May 1. Then, on Wednesday, a few comments from Vladimir Putin seemed to pop the bubble, and within a few days the Dutch TTF price was down 27%. Is everything OK now? Was the gas-price run-up all just speculative buying and short covering? Or is a supply crunch still on the horizon, and this is just the calm before the storm? In today’s RBN blog, we explore those questions.

- Blog

Break It to Me Gently - Factors Influencing U.S. LNG Offtaker Decisions to Lift vs. Cancel Cargoes

Global natural gas demand disruptions and high storage levels resulting from the COVID crisis have turned international LNG markets upside down. Price spreads for U.S. LNG exports, which were well above $1/MMBtu two months ago, have disappeared and even flipped to negative, with the UK NBP and Dutch TTF price benchmarks — and briefly also Asia’s JKM index — trading below the U.S. benchmark Henry Hub for the first time since the U.S. began exporting LNG in early 2016. Despite the uneconomic price spreads, U.S. cargo liftings have slowed only modestly so far. That’s likely to change in the coming months as both Cheniere Energy and Sempra have confirmed cancellations or modifications to lifting schedules by some offtakers, and other terminal operators are likely facing the same pressure. However, many U.S. cargoes will still move, regardless of prices. What are the economics of cancelling versus lifting a seemingly out-of-the-money cargo? Today, we begin a short series examining the factors affecting U.S. LNG cargo liftings.

- Blog

It's Too Late - Global Natural Gas/LNG Supply Squeeze Sets Stage for Record Winter Prices

Global natural gas and LNG prices have spent the summer going from high to higher to the highest on record. The major European indices hit post-2008, and then all-time highs multiple times throughout the summer — even surpassing Asian prices on a handful of days. At the same time, Asian prices have set all-time seasonal records and are now sitting just below the previous single-day high settle from this past January. Usually, as the weather cools heading into fall, so do prices, but that’s unlikely this year as the European gas storage inventory is at the lowest level for this time of year than we’ve seen in recent history, and the time to replenish stocks for the winter is rapidly running out. The incredible bull run for global gas prices has been underpinned by high demand for LNG and the cascading effect of a supply squeeze in Europe, brought on by the triple threat of low domestic production, decreased imports from Russia, and a scarcity of incremental LNG cargoes. Not only is this driving record-high gas prices and increased volatility now, but the low inventory means sustained high prices for the heating season ahead. In today’s blog, we take a look at recent global gas price trends and the precarious European storage situation ahead of what is shaping up to be an incredibly bullish winter.