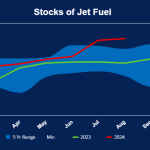

Gross refinery input for the total U.S. increased by 200 Mb/d last week, reaching 17.1 MMb/d and bringing capacity utilization up to 93.3%, the highest rate in six weeks. Motor gasoline demand rose by 100 Mb/d to 9.3 MMb/d, as inventories fell by 2.2 MMbbl. Distillate stocks increased by 275 Mbbl, primarily due to PADD 3 growing by 800 Mbbl. Finally, jet fuel inventories have surged since mid-June, now hovering around 5 MMbbl above the five-year maximum. Jet storage was already 2 MMbbl over the five-year maximum as of the week of July 8. The situation was exacerbated by the CrowdStrike software crash on July 19, which grounded flights globally for nearly a day.

Featured Articles

- Blog

Much Too Much - Distillate Glut Challenges U.S. Refiners But Offers Contango Opportunity

For the past several months, U.S. refineries have been producing more distillate than demand warrants, resulting in a glut of distillate fuels, especially ultra-low-sulfur diesel and jet fuel. The disconnect between supply and demand has been particularly stark in the Gulf Coast region, where just a couple of weeks ago distillate stocks sat 39% above their 10-year average after coming perilously close to tank tops in August. The culprit, of course, is COVID-19, or more specifically the effects of the pandemic on air travel and the broader economy. Demand for motor gasoline rebounded more quickly than demand for ULSD and jet fuel, and refineries churned out more gasoline to keep up, but that results in more distillate too. Now, finally, there are signs that distillate stocks may be easing back down. Today, we discuss the build-up in ULSD and jet fuel stockpiles, the ways they might revert to the norm, and the potential for storing distillate now and selling it at a higher price later.

- Blog

The Midwest Crack Spread Margins Really Make You Feel Alright!

Ever since US crude production began to increase in 2009 after 40 years of decline from its peak in 1970, refineries have been processing higher crude volumes. This summer (2014) crude processing volumes have been higher than at any time since the Energy Information Administration (EIA) began keeping records in 1982. Abundant supplies of reasonably priced crude in all regions as well as low refinery fuel costs are giving US refiners good reason to crank up their output. So much so that in the Midwest refinery output reached over 100 percent of capacity early in July. Today we describe the refining bonanza and how things might change in the not too distant future.

- Blog

Hot Fun in the Summertime - Petroleum Product Exports Riding High

We are getting into the peak summer driving season and gasoline demand has been hitting all-time highs. You might think that inventories would be drawing down and that the U.S. would need to import more gasoline and gasoline blending components. But not so. U.S. refineries are cranking out the products. Gasoline stocks are up 10% from a year ago—15 million barrels (MMbbl) higher than the top of the five-year range—and last week gasoline inventories made a contra-seasonal move upward, increasing by 1.4 MMbbl. Net exports for the first quarter were up almost five times the same period in 2015. But what does all this mean for refined product markets in general, and gasoline balances in particular? Today, we examine the state of U.S. petroleum product markets.