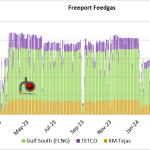

LNG Feedgas demand at Freeport LNG dropped below 1 Bcf/d on March 4 and has been below that level since. Freeport Train 3 is currently offline following damage to an electric motor incurred during the deep freeze in mid-January. Freeport initially said repairs would take about a month, but later delayed the restart by another two weeks, implying a mid-March restart. Flows to the terminal have been mostly consistent with two trains operating fully since the end of January, except for two additional unplanned restarts – one on February 6 and another on February 17. In both instances, feedgas rebounded the next day. It is unclear if the drop below 1 Bcf/d on March 4 is related to the restart or due to some other issue. Unplanned restarts at the terminal are typically reported to Texas state regulators as they cause an emissions event, but no new incidents have been reported since mid-February. Nonetheless, based on feedgas intake, only one train at Freeport appears to be operational just now.

Featured Articles

Freeport LNG Maintenance Work Continues

Shut Down - Gas Flow, Price Impacts of the Freeport LNG Outage

An explosion June 8 at Freeport LNG, the 15.3 MMtpa (2 Bcf/d) export terminal on Quintana Island, TX, has knocked it offline at a time when the global market is already facing tight conditions because of the war in Ukraine and other factors. The explosion, fire and subsequent shutdown — which fortunately did not include any injuries — sent U.S. natural gas tumbling off recent highs and shot global gas prices higher. Much is still unknown about the developing situation, including exactly how long the outage will last. While Freeport has said it expects the terminal to be offline for at least three weeks, multiple regulatory agencies have investigations underway and will likely need to approve a return to service. In today’s RBN blog, we look at the latest news from Freeport LNG and run through the potential market implications, starting with impacts to the U.S. gas market.

Better Days - U.S. LNG Feedgas Rebounds as Spring Maintenance Season Rolls Off

Global gas prices have had a record-breaking year so far, with JKM in Asia hitting all-time seasonal highs in spring, and TTF in Europe last week reaching the highest level since 2008. Prices have been spurred on by a global LNG market that is undersupplied and hunting for additional cargoes. If you were just looking at U.S. feedgas levels over the past several weeks, though, you would never know that we are in the middle of an incredible bull run. U.S. LNG feedgas deliveries have trailed below full-utilization levels for more than a month due to a combination of spring pipeline maintenance, LNG terminal maintenance, and operational issues. The reduced availability of pipeline and liquefaction capacity led feedgas deliveries in June to average 9.35 Bcf/d, or about 85% of full capacity. However, this was just a small and short-lived setback before what is likely to be a breakthrough summer for U.S. LNG. Feedgas demand is already back above 95% utilization and is poised to head even higher over the next few months both from new liquefaction capacity coming online and potentially from spot market cargo production. In today’s blog, we take a look at the impact of spring maintenance on U.S. LNG production and potential feedgas demand growth in the months ahead.