It is winter in propane country, and even though it has been a relatively mild one so far, propane prices have been remarkably weak. For one thing, the ratio of Mont Belvieu propane to WTI crude oil has been in the dumper all year, averaging a paltry 35% since March. Last year for the same period the ratio was 47%.

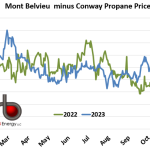

But up in the Conway, KS hub that feeds the largest propane market in the U.S. – the Midwest region, the price has been even cheaper. The graph below shows the Mont Belvieu minus Conway differential for the past two years with 2022 in green and 2023 in blue. Note that starting in September of this year, Mont Belvieu started moving higher than Conway, and it’s been ramping up ever since, getting to 5 cents/gallon on Friday (red dashed oval; Mont Belvieu was 72 c/gal. while Conway was 67 c/gal.)

So what’s going on? First, PADD 2 inventories – the Midwest/midcontinent region - are in great shape. EIA’s most recent weekly report showed stocks at 27.1 MMbbl, which is .75 MMbbl, or 2.8%, over the 5-year maximum. Second, the region has not seen a sustained bout of unusually frigid weather. Third, exports from the Gulf Coast have been strong, supporting propane prices in Mont Belvieu.

Although this year’s winter Mont Belvieu premium is noteworthy, it is certainly not unexpected. The average Mont Belvieu price is historically above Conway during the coldest months (December-February) about one-third of the time for the past 15 years. This year with strong Gulf Coast exports and robust PADD 2 inventories, it is clear that the only thing that would boost Conway above Mont Belvieu would be sustained cold weather in propane country. And so far, that has not happened.