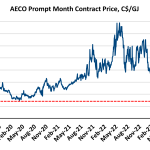

Canadian natural gas cash prices remain locked in sideways land as a persistent lack of weather-related demand strength has combined with above average storage levels and rebounding production due to the fading threat from Alberta wildfires. AECO forward prices, which had been able to partially withstand bearish price pressures until recently, have also begun to wilt with the prompt month contract price hitting lows not seen since summer 2019 and the COVID-driven lows in April 2020 (lows touching dashed red line in top figure below).

Featured Articles

- Blog

Extreme Ways - What It Took to Balance the Natural Gas Market This Fall

You wouldn’t know it from the $2.50-plus/MMBtu Henry Hub prompt natural gas futures prices in the past couple of months, but the U.S. gas market this injection season just barely managed to avoid a complete meltdown. Despite gas production volumes trailing year-ago levels all summer long, it wasn’t until the last month or two of the traditional injection season (April through October) that the market tightened enough to escape a major storage crunch. In reality, it took the multi-pronged effects of production cutbacks — in part from hurricane-related disruptions — higher LNG and pipeline exports, and cooler fall weather, to make that happen. Today, we review the U.S. natural gas supply/demand balance and implications for 2021.

- Blog

Summertime - Low European Stocks, High Global Gas Prices to Keep U.S. LNG Production at Full Capacity

U.S. LNG export terminals are running at their operationally available and contracted levels and will continue to do so, with no economically driven cargo cancellations anywhere on the horizon. Global gas prices are well supported by low storage levels in Europe, and it will take time to refill inventories, which means these high prices are not going away anytime soon. The upshot: U.S. LNG will have a very different kind of summer than it did last year, when global prices were at historic lows and many U.S. terminals saw more cargo cancellations than exports. Feedgas in April this year averaged 10.77 Bcf/d, nearly 3 Bcf/d higher than last year, and as we progress into summer, the year-on-year delta will become even more pronounced. Barring any major operational issues, feedgas demand will stay around 11 Bcf/d, which is the level needed for the terminals to produce at full capacity. That’s in stark contrast to last summer, when feedgas demand cratered and averaged as low as 3.34 Bcf/d in July as cargo cancellations peaked. Today, we look at what’s supporting global gas prices, how that impacts export economics for U.S. LNG, and what that means for feedgas demand in the months ahead.

- Blog

Don't Be Afraid - Low Alberta Gas Storage Is Not Spooking the AECO Winter Market, Yet

Alberta natural gas storage, one of the largest regional storage hubs in North America, is experiencing one of its slowest cumulative storage injection rates in years and could be headed to a 13-year low for storage levels by the end of the current injection season. That may seem ominous for the chilly Alberta and Canadian winter heating season, not to mention gas exports to the U.S. So far, though, winter gas forward prices for the Western Canadian gas price benchmark of AECO have registered a relatively modest market response, staying in line with last winter’s average spot price. Today, we take a closer look at the market’s apparent lack of concern over low Alberta gas storage.