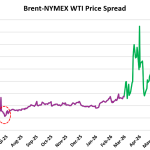

The world's two leading crude oil benchmarks, Brent and West Texas Intermediate (WTI), posted their steepest weekly declines in months during the week ended June 26 as traders unwound some of the geopolitical risk premium that has supported prices for much of the year. The broad weakness in crude benchmarks was accompanied by a sharp compression in the Brent-WTI spread. This Brent-WTI spread (also called “the arb”) represents the price difference between Brent (the global crude benchmark) and CME / NYMEX WTI (the U.S. crude benchmark representing Domestic Sweet Cushing).

Last week, Brent fell 10.6% to $71.99/bbl, while WTI fell 9.6% to $69.23/bbl. As discussed in this week's TradeView Report, both benchmarks fell below their 50-, 100-, and 200-day moving averages and settled Friday at their lowest levels since late February. After holding above $6/bbl and repeatedly reaching double digits for much of March through May (shown by the green portion of line in chart below), the adjusted Brent-WTI spread declined for much of June, narrowing to just $2.76/bbl last week (blue oval) before tightening further to $2.40/bbl on Monday. Excluding days of Brent expiration when price swings are commonly seen, this is the narrowest the arb has been since June 2025 (red oval).