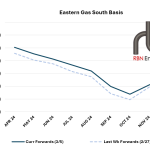

Forward prices at Eastern Gas South (EGS) have increased over the past week, as traders are increasingly pricing in the potential for sustained production cuts through the end of the year. EGS, formerly known as Dominion South, is an important hub for the Appalachian production region. While Henry Hub futures have been on the upswing over the past week, outright forward prices in the Appalachian production zone rose even more quickly, causing the basis discount to narrow.

Featured Articles

- Blog

Danger Zone - The Outlook for the Appalachian Natural Gas Market

It’s been a while since the Appalachian natural gas market has looked this bullish. Outright cash prices at the Eastern Gas South hub are at multi-year highs. Regional storage inventories are sitting low, setting the stage for supply shortages and still higher prices this winter. But the potential for severe takeaway constraints and basis meltdowns are lurking, and by next year, they could become regular features of the market again like they were in the 2016-17 timeframe, or worse — at least in the spring and fall when Northeast demand is lowest. Regional gas production is still being affected by maintenance and has been somewhat volatile lately as a result, but it averaged 34.5 Bcf/d in June, just 300 MMcf/d shy of the December 2020 record. What’s more, at current forward curve prices, supply output could surpass previous highs by next spring and grow by ~ 5 Bcf/d (15%) by 2023. Outbound flows set their own record highs this spring, running at over 90% of takeaway capacity, and will head higher, which means that spare exit capacity for supply needing to leave the region is shrinking. The handful of planned takeaway expansions that remain are facing environmental pushback and permitting delays, and the few that are targeting completion in the next year may not be enough. Today, we provide the highlights of the latest forecast from our new NATGAS Appalachia report.

- Blog

It's a Hard Knock Life - Appalachia Gas Outflows, Prices Take a Hit with TETCO Capacity Cut

This year has been a mixed bag for Appalachian natural gas producers. Outright prices in the region are higher than they’ve been in a few years, thanks to lower storage inventory levels and robust LNG export demand. However, regional basis (local prices vs. Henry Hub) is weaker year-on-year as higher production volumes have led to record outbound flows from Appalachia and are threatening to overwhelm existing pipeline takeaway capacity. Last month, Equitrans Midstream officially announced that the start-up of its long-delayed Mountain Valley Pipeline (MVP) project will be pushed to summer 2022 at the earliest. Then, just last week, outbound capacity took another hit as Enbridge’s Texas Eastern Transmission (TETCO) pipeline was denied regulatory approval to continue operating at its maximum allowable pressure, effectively lowering the line’s Gulf Coast-bound capacity by nearly 0.75 Bcf/d, or ~40%, for an undefined period. Today, we consider the impact of this latest development on pipeline flows, production, and pricing.

- Blog

We Can Work It Out - Appalachia Gas Basis Outlook in a Pipeline-Constrained World

Appalachian natural gas producers and marketers are adapting to a new status quo — a world where new pipeline takeaway capacity out of the Northeast is hard to come by and is more or less capped ad infinitum. Without the assurance of pipeline expansions, regional gas producers are no longer drilling with abandon in hopes that the capacity will eventually get built. Instead, producers are practicing restraint by slowing drilling activity, delaying completions and choking back producing wells to manage their inventory during periods of lower demand and prices. In today’s RBN blog, we consider what this new playbook will mean for pricing trends in the supply basin.