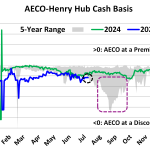

During much of June and early July 2025, the AECO-Henry Hub cash basis has been trending at its lowest levels in more than two decades (chart below). As described in RBNs’ Canadian NatGas Billboard, the basis, or price differential that separates the cash price of natural gas at the Henry Hub in Louisiana and the cash price of natural gas at the AECO Hub, Western Canada’s primary natural gas price marker in Alberta, has frequently been lower than $(2.00)/MMBtu (blue line) since June and was recorded as $(2.36)/MMBtu on July 8 (black dashed circle). These are levels that have often been lower than the five-year range (gray shaded area) and, at times, lower than any basis value recorded since 2000 for this time of year.

Featured Articles

- Blog

AECO Prison Blues - Western Canadian Gas Prices Stuck Behind Bars, Even After Winter Price Surges

Western Canada’s natural gas market never really seems to catch a break. Prices this winter have remained well below those across much of the rest of North America thanks to an all-too-common combination of insufficient pipeline export capacity from the region, bloated gas storage and robust supply growth. Even with forward price prospects for much of the rest of the continent looking buoyant, with more gas expected to head to expanding Gulf Coast LNG terminals and a storage-refill season that will be stronger than last year, price upside for Western Canada looks to be minimal at best and will be partly dependent on the rate of gas intake to LNG Canada, as we explain in today’s RBN blog.

- Blog

Money, Money, Money - Canadian Gas Producers Pivoting Toward Greater LNG Price Exposure

For the past several years, Western Canada’s natural gas producers have been forced to sit on the sidelines of too many broader price rallies as their main benchmark, AECO, languished at painfully low levels. Though an increasing number of producers have been steadily diversifying their price exposure away from Western Canada and AECO, even greater pricing upside might be captured if marketing arrangements could be developed to access higher international LNG prices via U.S. Gulf Coast terminals. In today’s RBN blog, we look at the steps that two of Canada’s largest natural gas producers have taken to capture that LNG price upside.

- Blog

Get Me Out of Here, Part 2 - Western Canada's Natural Gas Production is Nearing All-Time Highs

Once consigned to a flat or declining profile, natural gas production in Western Canada has been increasing steadily since 2012, to the extent that it has now begun to stretch the ability of the existing pipeline network to the breaking point. Most striking is that this expansion in production has been taking place in an era of declining natural gas prices and weakening basis for Western Canada’s primary natural price marker, AECO, and rising and relentless competition from U.S. gas supplies in several of Canada’s key domestic and export markets. If the pricing, pipe egress and export situation has become so dire, why are producers still drilling for and pumping out even more natural gas? Today, we address this question in the second part of our series investigating Western Canada’s natural gas supply and demand balance.