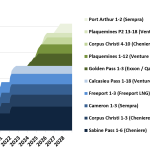

With Sempra's Port Arthur LNG and Venture Global's Plaquemines P2 achieving Final Investment Decisions (FID) in the last two weeks, the outlook for Texas and Louisiana natural gas needed to feed all of the existing and planned terminals ratcheted up to nearly 21 Bcf/d in 2027. About 8 Bcf/d higher than what we see when the current fleet of terminals is operating at full capacity.

Featured Articles

- Blog

All Shook Up - Arrow Model Forecasts Shifts in Gas Flows, Basis as New Pipes, LNG Capacity Arrives

The rapid growth in U.S. natural gas production and LNG exports over the past 10 years was just the beginning. Between now and 2035, gas production in the Permian, Eagle Ford, Haynesville and other plays will continue rising, the Gulf Coast’s LNG export capacity will double and many new pipelines will be built. New gas-fired power plants will be added, too. The shifts in gas flows as new production and infrastructure come online will be frequent and often sudden, as will the changes in basis at gas hubs throughout Texas and Louisiana. Is there any way to make sense of it all? There sure is. In today’s RBN blog, we continue to explore how our Arrow Model helps guide the way.

- Blog

Where It's At, Part 2 - Timing Is Everything for Gulf Coast Gas Producers, LNG Offtakers

As U.S. LNG export project development accelerates along the Gulf Coast, one of the big uncertainties is where will all that feedgas come from? We estimate that there are a dozen Gulf Coast projects totaling 16 Bcf/d of export capacity in the running for completion in the next decade, with 60% of that capacity sited along a less-than-100-mile stretch of coastline straddling the Texas-Louisiana border. One of the major factors that will influence the timing and commercialization of the projects is the availability of feedgas supply where and when it is needed. With pipeline projects and production growth in the Marcellus/Utica shales at a veritable standstill, the Texas and Louisiana production regions — the Permian, Eagle Ford and Haynesville — are the frontrunners for serving the bulk of the resulting Gulf Coast demand growth. Assuming no midstream constraints, RBN’s Mid-case production forecast anticipates growth from the three basins will total 15.5 Bcf/d by 2032. In today’s RBN blog, we look at how well (or not) production levels will line up with feedgas demand.

- Blog

Gotta Get Over, Part 2 - Southwest Louisiana Gas Pipeline Projects Targeting LNG Export Demand

As U.S. LNG export project development accelerates in the coming years, a lot more natural gas pipeline capacity will be needed to supply the numerous liquefaction facilities vying for a piece of the global gas market pie. That’s particularly true for a small stretch of the Gulf Coast from the Sabine River on the Texas-Louisiana border to the Calcasieu Pass Ship Channel — where the bulk of planned export capacity additions are concentrated — even as transportation bottlenecks are emerging for getting natural gas supply to the area. To address the growing demand, a number of pipeline expansions are planned or proposed to bring more supply into the region or deliver feedgas across the “last mile” to these multibillion-dollar facilities. In today’s RBN blog, we continue our series highlighting some of these LNG-related pipeline projects, this time focusing on ones aiming to feed exports out of southwestern Louisiana.