On Thursday of last week I spoke at the Colorado Oil & Gas Association (COGA) ‘Energy Epicenter’ conference in Denver. The topic for our panel was Crude and Mid-Stream Liquids, and was focused on the opportunities and challenges inherent in the rapid growth of U.S. crude oil and NGL production, both in the Rockies and across the country. In response to a number of requests, I have summarized my presentation in today’s blog.

COGA is a large conference held each year that brings together just about everyone involved in the Oil & Gas business in the Rockies. It was held this year Aug. 13-16 at the Colorado Convention Center in Denver. I had the honor of speaking on a panel with several distinguished leaders of the Rockies midstream industry: Tom O’Connor, CEO, DCP Midstream Partners, Pierce Norton, COO, ONEOK, and Don Sinclair, CEO of Western Gas Partners. Our moderator was Steve Jones, Managing Director, Tudor, Pickering. Each of us did a short 10 minute presentation and then we took questions from the audience.

Note: Some of the slides are included here, but not all. A full pdf of the powerpoint deck is attached. Some RBN Members have had problems downloading files from the RBN website. If you have trouble with this one, please email [email protected] and we will email a copy to you.

Introduction

Thank you Steve. Since we are going to focus primarily on the Rockies during the Q&A, I thought it would be helpful to set the context for our discussion of crude oil and NGLs at a more macro level. In both markets we are dealing with regional surpluses in this country – producing more than we can use. And that situation is likely to continue for years to come. The big question is – Where will all that supply find a home?

The NGL Story

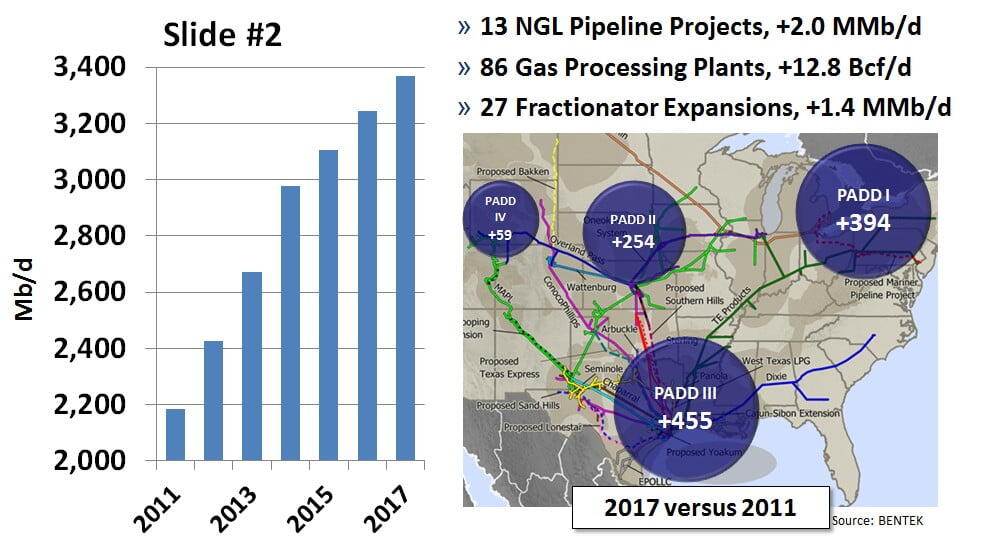

Let’s first start with the NGL story. (see Presentation Slide #2 & below) Gas plant production of NGLs is up from 1.7 MMb/d in 2007 to about 2.2 last year, and up again to 2.4 MMb/d today. The most recent Bentek forecast shows that number getting to nearly 3.4 in 2017, or 1.2 MMb/d over last year. This graphic shows where the growth is coming from. By far the biggest percentage growth is PADD I – the Marcellus and Utica - up 394 MB/d. The Gulf will see an increase of 455 Mb/d, PADD II which includes the Bakken up 254 Mb/d and here in the Rockies only 59 Mb/d.

To get all of that production to market, 13 pipeline projects are being developed for a total increase in supply of 2 MMb/d. Over 70% of that capacity will be used to bring product to the Gulf Coast, which is where most of the demand growth is located. 86 gas processing plant projects are in the works, increasing processing capacity by 12.8 Bcf/d. And there are 27 new fractionators or expansions being built, increasing that capacity by 1.4 MMb/d. That’s a lot of infrastructure.

Where will all of these surplus NGLs find a home? We’ll need to look at each of the products individually.

(Slide #3 & below) Ethane markets will be oversupplied until new crackers startup in 2017. It is the fastest growing NGL product, and even though there are a lot of petrochemical plants being debottlenecked, for the next few years they probably will not be able to keep up with production. By 2017 there will be several new – and very large chemical plants built. Until then the supply/demand balance will periodically move through oversupply cycles: new ethane production in excess of demand comes online --- then incremental petrochemical capacity expansions work off the production --- then more production starts up. It will get particularly bad in 2015 and 2016 when it is likely that ethane producers will run significantly ahead of demand. As shown here, 2016 ethane supply will be just under 1.5 MMb/d while U.S. ethane demand will only be about 1.3 MMb/d. The balance will either be exported to Canada (some from Marcellus, some from Bakken) or the ethane will be rejected – sold as natural gas for lack of market. As we’ve discussed before, ethane rejection implies the price of ethane will decline to a fuel value equivalent at the plant tailgate (see Nowhere to Run).

Comments

Rusty -

First, let me just say that I enjoy your posts (really all the ones at RBN) and have learned more from them than any other source that I can think of.

Second, a small suggestion: When you write a series of posts, I notice that you put in links in each post to refer to the previous posts. What would be nice would be go to the PREVIOUS POSTS and put in links to the SUBSEQUENT ones. That way, it'd be easy to pick up the thread no matter where one is. This is all the more important since the posts (even when they are named Part X) in a series don't always have the same title.

Now for the question about goodness and mercy, but mostly about sweetness and light: Yes, it's technically true that US production is getting lighter (bad, Eagle Ford!) and a tad sweeter. But, as a practical matter we do need to think of production from the northern suburbs of the U.S. (that's Canada) as part of that same mix. When you include Canada in the mix does the sweetness and light thesis break down?

I think the 'sweetness and light' thesis is true only if you believe that production in Venezuela and Mexico are in RAPID and terminal decline... if that's the case it'd be good to come out and say so. If not, I think that what we have is net growth in heavy and heavy sour crude in domestic'ish' (which includes Canada) production through 2017-2020 and, under those circumstances, maybe some of the refineries on the Gulf Coast (I'm thinking Valero here) don't look as overinvested in complexity as they might otherwise appear.

Please enlighten,

AZM

In reply to Questions about 'Sweetness and Light' by Aslam Mukhtiar

I should clarify that the question is really not so much whether or not US production is getting sweeter and lighter (that much is true), but that when taken in the context of what's going on in Canada, Venezuela and Mexico (all together) do you still think that US Gulf Coast refiners will find themselves with a deficit of heavy /sour at an appropriate enough discount so much so that they'll be regretting having invested in complexity?

This is really an informative post. It seems like US Gulf Coast refiners are making good wealth in crude oil production.

fonds de commerce