The CME/NYMEX Henry Hub natural gas futures contract turns 25 years old this year. The contract is now the third largest physical commodity futures market in the world. The price of virtually every Btu of gas sold in North America is linked in some way to the underlying physical hub at Henry. But over the past five years shale gas has revolutionized North American supply and changed the shape of delivery patterns. These trends have altered the flow of physical gas through Henry Hub and could jeapordize the success of the futures contract. Today we look at why Henry Hub has been so successful.

In Part I, we recounted how Henry Hub was chosen as the delivery point for the CME/NYMEX natural gas futures contract shortly after deregulation of the physical gas market encouraged growth in spot trading in the late 1980’s. We noted that Henry is not actually a hub, but a series of interstate interconnects with the Sabine pipeline in Southern Louisiana. What made it so attractive to the founders of the NYMEX contract was that Henry provided a strong physical basis for the financial market they were trying to create. This physical-financial relationship is critical to a successful futures contract because it ensures that futures prices are grounded in reality. This time we look more closely at some of the criteria that have helped make the Henry Hub futures contract so successful. Understanding these factors will help us assess the viability of the Henry Hub contract in a changing market going forward.

Futures contracts are a specialized form of “insurance” that allow market participants to manage their exposure to price risk. In their present form – organized exchanges – futures markets have been around for 160 years starting with the Chicago Board of Trade in 1848. Futures exchanges offer specific contracts for trading – in our case the Chicago Mercantile Exchange (CME) trades Henry Hub Natural Gas Futures Contracts. The Natural Gas Contract at Henry Hub is listed by the CME for as many as 155 future delivery months into the future (current year plus 12 years forward). Futures market participants buy and sell “paper” contracts on the CME, which permit them to take delivery of (buy) or make delivery of (sell) standard quantities of natural gas during a particular month in the future at the contract delivery point – Henry Hub. In the case of natural gas futures the standard contract unit is 10,000 MMBtu. Technically the settlement of standard CME Natural Gas Futures contracts is accomplished by physical delivery of the commodity at Henry Hub. In reality, only a small percentage are held by participants “to expiry,” meaning that the holder intends to make or take physical delivery. The vast majority of these paper contracts (~98%) never actually result in delivery, because they are offset by a matching buy or sell transaction in the futures market before the delivery period occurs. Regardless of whether futures contracts are physically fulfilled or not, the delivery mechanism provides a critical link between the futures contract and the underlying physical spot market. The following characteristics help determine the success of the natural gas futures contract physical delivery mechanism :

- Liquidity in the underlying spot market: Liquidity means that many different participants trade the commodity in the physical market and that there are high numbers of transactions. Liquidity allows participants to enter and exit a market easily by finding a trading partner. Liquidity also prevents one or a few participants from dominating the market. Liquidity is characterized by a wide range of participants ideally with different perspectives such as producers and consumers. As we have seen, Henry Hub has a large number of market participants and is among the most liquid trading locations in the US natural gas market.

- Fungibility in the underlying commodity: Fungibility is not the green stuff that develops on your cheese when you leave it outside the refrigerator. Fungibility means a commodity is widely available in a particular form or quality specification that market participants can agree upon and comfortably trade between them. If a commodity is not fungible then it is harder to trade and liquidity is constrained. Fungibility has two elements – physical specification and business process. Physically, natural gas is fungible at Henry Hub because it has to adhere to standard pipeline quality specifications. In general natural gas pipeline specifications throughout the US do not differ materially, particularly because gas is priced based on heating content ($ per MMbtu, or millions of BTUs). Heating content may vary, but pricing according to heat content ‘trues that up’. Thus, one molecule of gas can be substituted easily for another, which makes deliverability easier.Fungibility at Henry Hub is further facilitated by by an imbalance agreement between the pipelines involved that simplifies the transaction process.

- Price convergence between physical and financial markets: Physical-financial price convergence helps stabilize the futures contract and keep price movements more efficient because they are grounded in fundamentals. The delivery mechanism allows futures and physical market prices to converge as the expiration date of a futures contract approaches. The expiration date is the last day that the exchange allows trading for a futures contract – in the case of CME natural gas this is usually three business days before the end of the month before delivery. If a futures contract holder retains an open position until the expiration date, then their paper contract becomes physically deliverable during the contract month. It follows therefore that – as the expiration date approaches - the price of the contract for future delivery will converge with the price for physical delivery (aka the spot market price). And on the day that the physical gas is delivered at Henry Hub, its value will be essentially the same as any other spot market transaction at the Hub for delivery that day. A lack of convergence signifies that the price of a futures contract has become untethered from the physical reality of the delivery hub, meaning that counterparties would effectively be taking on additional, unpredictable risks associated with the difference between futures and spot prices.

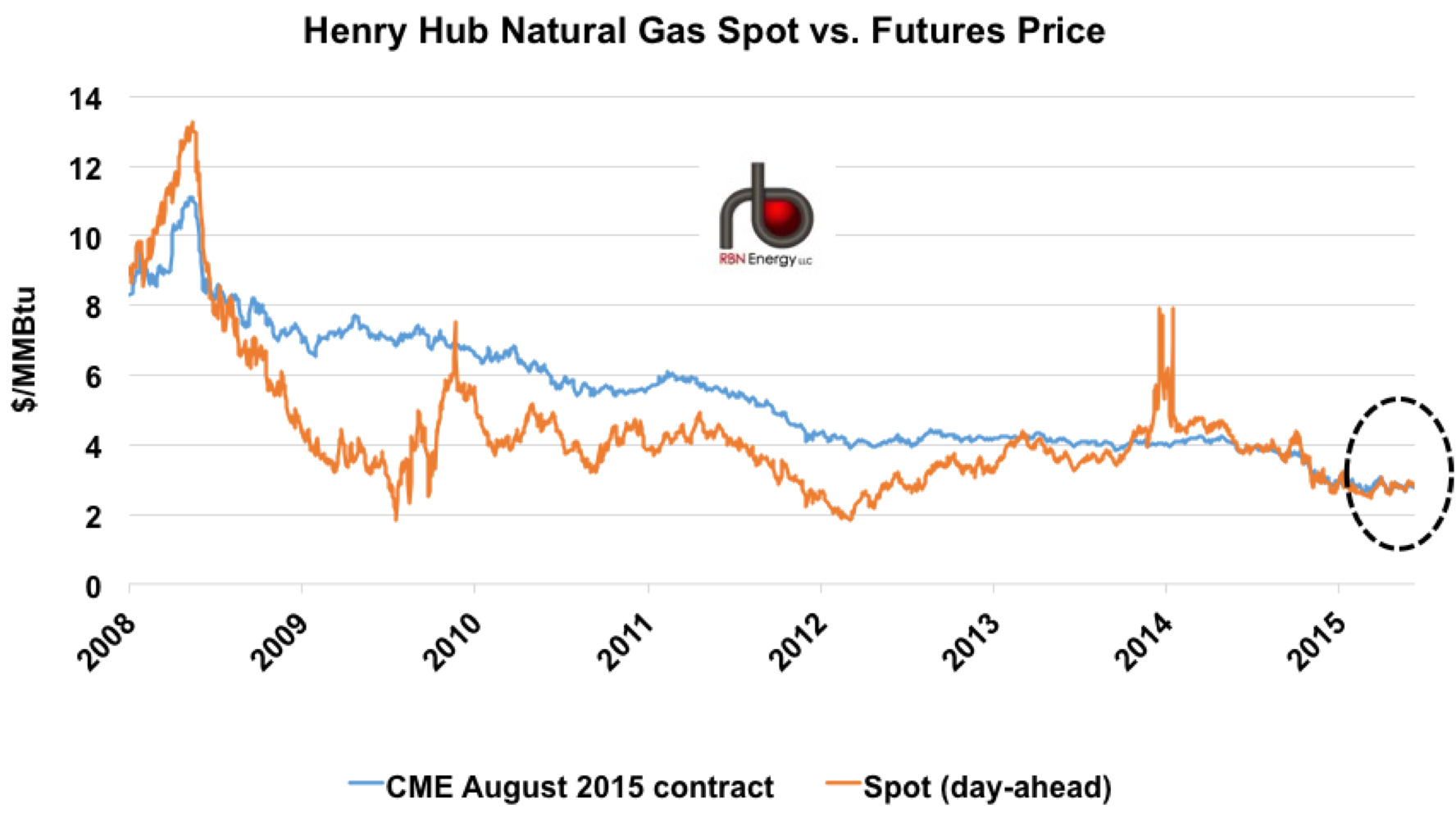

The chart in Figure 1 shows how prices for August 2015 gas futures converged with the underlying Henry Hub spot price as the expiration date (July 29, 2015) approached. The blue line represents daily settlement prices for the Henry Hub August 2015 futures contract, while the orange line is the day-ahead NGI spot price for Henry Hub, both in $/MMBtu. The August 2015 contract began trading as far back as 2008. Through 2012, its price difference to the spot market averaged $1.815/MMBtu. The gap began narrowing a bit in 2013 and 2014, when it averaged $0.42 and $0.44/MMBtu, respectively. This year the gap has averaged just $0.10 and in its final month of trading, less than $0.05 of spot prices (black dashed circle). The futures contract expired yesterday – settling at $2.886/MMBtu, just $0.015 under the same day’s spot price average of $2.901/MMBtu.

Figure 1; Source: CME data from Morningstar, NGI

About the song

I Am Henry VIII I Am was originally written back in 1910 for a British Music Hall act but became a #1 Hit on the Billboard 100 in 1965 for Herman’s Hermits.