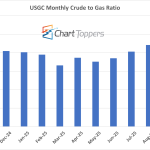

The NYMEX crude-to-gas ratio for October 2025 — shown by the green bar in the chart below — stands at 18.6, down from 21.3 in September, with crude at $59.89/bbl and gas at $3.25/MMBtu. By contrast, October’s ratio is still notably lower than a year ago, at 28.1 in October 2024 — represented by the red bar — when crude was $71.86/bbl and gas was $2.58/MMBtu. That’s a 13% decline from September and about 34% lower year-on-year, reflecting how softer crude prices and firmer gas fundamentals have narrowed the ratio heading into late 2025.

Featured Articles

- Blog

Oil-Weighted E&Ps' Capex and Production

<h3 style="margin-bottom: 0;">E&D Capex ($MM)</h3><table border="0" cellpadding="0" cellspacing="0" class="tablesaw tablesaw-swipe" data-tablesaw-mode="swipe" data-tablesaw-sortable style="font-size: 10px;">

<thead>

<tr style="background-color: steelblue; color: white; font-weight: 900;">

<th></th></tr></thead></table>

- Blog

Big Machine, Part 3 - E&Ps' Second-Quarter Profit Growth Squelched by Stagnant Realizations

The U.S. exploration and production sector has reaped many benefits from its transformation to large-scale, manufacturing-style exploitation of premier resource plays, generating record oil and gas production while slashing production and reserve replacement costs by 50%. While increased efficiency and rising output have moved the industry solidly into the black after three years of losses, profit growth stalled in the second quarter 2018 despite a $5/bbl increase in oil prices to about $68/bbl. The cause is largely beyond the control of the producers: constraints on getting the increased output to markets. In certain producing regions, most notably the Permian Basin, production growth has far outpaced expansions to the infrastructure required to process and transport it. Today, we explain why these constraints are critical to assessing the outlook for industry profitability and cash flow over at least the next two to four quarters.

- Blog

Calm Before the Storm - E&P Q1 Earnings Rise Before Price Drop Darkens Q2 Outlook

Buoyed in part by early optimism about the Trump administration’s potentially positive impact on the economy and the oil and gas industry, the WTI spot oil price reached a five-month high of nearly $76/bbl in January. But the optimism and oil prices have steadily eroded due to the impact of tariffs, trade wars and stubborn oilfield service inflation. In today’s RBN blog, we’ll look at the impact of the January price spike on Q1 2025 earnings and analyze the potential impact of a much lower price scenario in Q2 2025.