Since Russia began its large-scale invasion of Ukraine in February 2022, interruptions in the flow of Russian natural gas to Europe have roiled energy markets on the continent – and created new opportunities for U.S. LNG exporters. The great majority of Russian pipeline exports to the continent were halted in 2022. Most of the Nord Stream system under the Baltic Sea was destroyed in September 2022. Flows from Russia through a pipeline in Belarus also trickled to a halt through the course of that year. Now a third route for Gazprom to sell gas into Europe is no longer operational, as the contract allowing Russia to transport gas on a pipeline through Ukraine expired at midnight on December 31. The Ukrainian government chose not to renew the contract, hoping that denying Russia a market for their gas will hurt the Russian economy and damage that country’s ability to prosecute the war.

Featured Articles

Turn The Page - EU's Efforts to End Reliance on Russian Natural Gas Could Boost U.S. LNG Exports

The European Union (EU) has had to rethink and reconfigure major elements of its policies around natural gas since Russia’s invasion of Ukraine in February 2022. Prior to the war, Russian volumes accounted for 45% of the EU’s imports of natural gas, nearly double the supply from second-place Norway, but Russian gas supplies have dropped considerably since then, impacting the global LNG market. In today’s RBN blog, we look at the EU’s continued efforts to reduce its reliance on Russia, how it’s trading supply risk for price risk, and what the changes could mean for U.S. LNG exporters.

You Don't Own Me - What Will It Take for Europe to Give Up Russian Gas?

The fallout from Putin’s full-scale invasion of Ukraine has been multifold, with the human tragedy front and center. But it’s also reverberated across world economies as governments move to sanction Russia and corporations cut their ties with it. In a bid to minimize the impact on energy supplies and prices, the U.S. and its European allies have been grappling with how best to wean themselves from Russian crude oil and natural gas. That was relatively easy for the U.S. — the Russian import ban announced earlier this week by President Biden is likely to have only minor side effects. But the challenges for Europe are far greater due to its significant dependence on Russian supplies. If you’re stateside and trying to make sense of the market implications of all that — and trying to wrap your head around Europe’s energy infrastructure (and its approach to discussing energy volumes) — you’re not alone. In today’s RBN blog, we begin a look at what the European response could mean for the global LNG market.

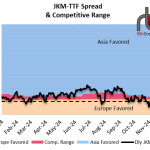

It's Too Late - Global Natural Gas/LNG Supply Squeeze Sets Stage for Record Winter Prices

Global natural gas and LNG prices have spent the summer going from high to higher to the highest on record. The major European indices hit post-2008, and then all-time highs multiple times throughout the summer — even surpassing Asian prices on a handful of days. At the same time, Asian prices have set all-time seasonal records and are now sitting just below the previous single-day high settle from this past January. Usually, as the weather cools heading into fall, so do prices, but that’s unlikely this year as the European gas storage inventory is at the lowest level for this time of year than we’ve seen in recent history, and the time to replenish stocks for the winter is rapidly running out. The incredible bull run for global gas prices has been underpinned by high demand for LNG and the cascading effect of a supply squeeze in Europe, brought on by the triple threat of low domestic production, decreased imports from Russia, and a scarcity of incremental LNG cargoes. Not only is this driving record-high gas prices and increased volatility now, but the low inventory means sustained high prices for the heating season ahead. In today’s blog, we take a look at recent global gas price trends and the precarious European storage situation ahead of what is shaping up to be an incredibly bullish winter.