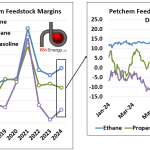

Margins for U.S. Gulf Coast steam crackers that make ethylene, propylene and other petrochemical intermediates out of natural gas liquids are the highest they have been since March 2022. As shown in the right graph below, since January 2024, the margin for ethane has doubled, from 12 c/lb to 24 c/lb, propane is up eight-fold, from 2.2 c/lb to 17.5 c/lb, while natural gasoline (light naphtha) has soared from negative 4 c/lb to positive 9.5 c/lb.

Featured Articles

- Blog

Ethylene Ethylene, Prettiest Margin I Ever Seen - Ethylene Margins Skyrocket; How Long Will It Last?

How about some good news to start the year? Over the past few weeks, ethylene margins have blasted into the stratosphere. These are good times for steam crackers, those petrochemical plants that use mostly NGL feedstocks to produce ethylene and other building-block chemicals. As you might expect, this newfound prosperity has a lot to do with ethylene’s price. In December alone, the price of ethylene was up 50%; versus April it’s up a whopping 4X, coming in yesterday at 37.5 cents per pound (c/lb). There are a whole range of factors responsible, including petchem outages due to the hurricanes, new downstream derivative units coming online, robust exports from the Enterprise Morgan’s Point dock, and, oh yes, strong demand for downstream products — everything from food packaging to construction materials. Is the spike in ethylene prices going to last? And what does it mean for NGLs, which account for more than 95% of the feedstock supply for U.S. ethylene. We’ll explore those questions and more in this blog series we begin today.

- Blog

Return to the Ethane Asylum - Price Skyrockets as Supply/Demand Uncertainty Looms for the Lightest NGL

That crazy little ethane molecule is at it again. Yesterday the price blasted to 67.875 c/gal, a level last seen on January 17, 2012. Petchem cracker margins are low. Production is up, but inventories are down. A big driver of the bedlam is the price of natural gas, trading in the $7-$9/MMBtu range for the past month. But as usual with ethane, there’s a lot more happening below the surface — including high domestic demand, growing export volumes, and significant developments in downstream petrochemical markets — all shaking things up. Looking ahead, uncertainty looms, with more export capacity, ever-changing ethane rejection economics, and uneven production growth. In today’s RBN blog, we’ll leap back into the ethane market to see what’s been going on, and where ethane is headed over the next few years.

- Blog

You're the One That I Want - RBN's Steam Cracker Feedstock Model And Its Uses

Every day, about 1.8 million barrels of NGLs, naphtha and other ethylene plant feedstocks are “cracked” to make both ethylene and an array of petrochemical byproducts. And every day, decisions are made for each steam cracker on which feedstock—or mix of them—would provide the plant’s owner with the highest margins. Within each petchem company, these decisions are optimized by staffs of analysts and technicians using sophisticated and complex mathematical models that consider every nuance of a specific ethylene plants’ physical capabilities. Fortunately for us mere mortals, it is possible to approximate these complex feedstock selection calculations for a “typical” flexible cracker using a relatively simple spreadsheet model. Today we continue our series on how the raw materials for ethylene plants are picked with an overview of RBN’s feedstock selection model, a review of feedstock margin trends, and an explanation of how the model also can be used to indicate future NGL and naphtha prices and to assess the prospects for various industry players.