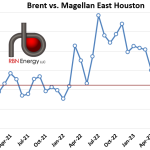

The spread between the price of Brent crude and Magellan East Houston is down to an average of only $2.35/bbl so far in October, a level not seen since May 2022, and as shown in the graph below is now more typical of the average monthly differential in 2021 (red line). The differential blew out following Russia’s invasion of Ukraine on February 24, 2022, peaking at $5.85/bbl in July 2022 as export bans and sanctions disrupted oil shipping, increasing rates and forcing inefficient routings.

However, in late 2022 the oil market started to normalize, shipping rates moved lower, and the differential narrowed. It is likely that Midland WTI deliveries into the Brent complex which started in May 2023 is also contributing to the narrowing differential. The differential dropped to a low of $1.75/bbl for one day at the end of September.

The big question is how the narrowing differential will impact export volumes. During the week of September 29, RBN’s Crude Voyager report showed that exports slowed to only 3.8 MMb/d, down nearly 1.5 MMb/d from the previous week. If the differential remains narrow and export volumes remain low, it will be an indication that the differential continues to be a good indicator of export economics. On the other hand, if exports move back to recent high levels, it would suggest that WTI Midland deliveries into Brent have impaired the relevance of the Brent marker price.