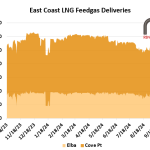

The Cove Point LNG facility in Maryland returned from its annual maintenance outage this past Saturday, and the facility has taken in 0.8 Bcf/d of natural gas on each day since returning. Cove Point took almost no feedgas during the 21 days between September 20 and October 11 (see the large dip in the dark orange section of the graph below), leaving the supply-demand balance looser during those three weeks. Domestic demand for natural gas is already low during this time of year – known as the shoulder season – when temperatures tend to be pleasant so both air conditioning and heating are used sparingly. This is a great time for LNG maintenance because demand for gas in Europe and Northeast Asia is also low, but in the domestic market it lowers demand when the balance is already loose.

Featured Articles

You've Got Your Troubles, Part 3 - Seasonal Demand Declines, Production Curtailments Hit Appalachian Gas Market

As U.S. natural gas spot and futures prices retreated in the past week, the price of gas at Appalachia’s Dominion South hub fell as low as $0.735/MMBtu, the lowest since fall 2017, before partially rebounding yesterday to about $1.10/MMBtu, according to the NGI daily gas price index. Moreover, the forwards market indicates sub-$1/MMBtu prices are in store for October as well. The regional supply hub didn’t weaken quite as much as prices at the national benchmark Henry Hub, which collapsed in recent days on demand losses — from cooler weather, storm-related power outages, and disruptions to LNG exports — and storage levels in the Gulf Coast region that are well above average and approaching peak capacity levels. The relative support for prices in the Northeast is in part due to a second round of production shut-ins by EQT Corp., which took effect September 1. But seasonal demand declines are underway; the Dominion Energy Cove Point LNG facility in Maryland just went offline for its annual fall maintenance, placing additional pressure on already-packed storage fields and takeaway pipelines; and pipeline maintenance events are reducing outflow capacity and curtailing production. Altogether, that signals more volatility ahead. Today, we provide an update on the fundamentals driving the Northeast gas market.

It's a Hard Knock Life - Appalachia Gas Outflows, Prices Take a Hit with TETCO Capacity Cut

This year has been a mixed bag for Appalachian natural gas producers. Outright prices in the region are higher than they’ve been in a few years, thanks to lower storage inventory levels and robust LNG export demand. However, regional basis (local prices vs. Henry Hub) is weaker year-on-year as higher production volumes have led to record outbound flows from Appalachia and are threatening to overwhelm existing pipeline takeaway capacity. Last month, Equitrans Midstream officially announced that the start-up of its long-delayed Mountain Valley Pipeline (MVP) project will be pushed to summer 2022 at the earliest. Then, just last week, outbound capacity took another hit as Enbridge’s Texas Eastern Transmission (TETCO) pipeline was denied regulatory approval to continue operating at its maximum allowable pressure, effectively lowering the line’s Gulf Coast-bound capacity by nearly 0.75 Bcf/d, or ~40%, for an undefined period. Today, we consider the impact of this latest development on pipeline flows, production, and pricing.

Turn the Page - Producer Restraint, Tighter Balances Disrupt Appalachian Gas Market Trends

Before the bullish winter of 2021-22, it appeared the Northeast natural gas market was headed for familiar territory: worsening seasonal takeaway constraints and deeper, constraint-driven price discounts starting as early as this spring. Instead, the market went in the other direction the past few months. Takeaway utilization out of Appalachia has been lower year-on-year and, for the most part, Appalachian supply basin prices have followed Henry Hub higher even as that benchmark rocketed to 14-year highs. That’s not to say that constraints out of the Northeast aren’t on the horizon. But the market is now poised to escape the worst of it this year, despite the completion of the last major takeaway pipeline project in the region, Mountain Valley Pipeline (MVP), being pushed out another year or longer, if it crosses the finish line at all. In today’s RBN blog, we provide an update on regional fundamentals and what recent trends mean for gas production growth and pricing in the region.