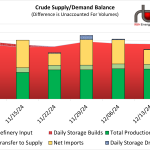

Happy holidays all. Net refinery input increased by 200 Mb/d to 16.82 MMb/d (red area in graph below), a bullish sign as refinery demand recovers much of its losses from previous weeks and nears the psychologically important 17 MMb/d threshold. Net imports rose by 1 MMb/d to 2.75 MMb/d due to a decline of 1.175 MMb/d in exports while imports fell by just 175 Mb/d. Although total supplies remained mostly flat at 14.14 MMb/d (green bar segments in graph below), a 4.2 MMbbl drop in inventories occurred (blue bar segments in graph below), primarily obscured by a 1.27 MMb/d swing in unaccounted-for volumes. Meanwhile, WTI prices stayed within a narrow range but ultimately declined, driven by disappointing economic data from China and pessimism about future U.S. economic growth following the Federal Reserve's announcement of fewer interest rate cuts than anticipated.

Featured Articles

One Piece at a Time - U.S. Crude Oil Supply/Demand Balances, Inventories and Pricing

Last week, crude oil prices dropped below $50/bbl, in part due to continued increases in U.S. crude oil inventories, and fell further over the next few days. Then yesterday, prices perked up by $1.14 to $48.86/bbl; again one of the factors was the weekly inventory number from the Energy Information Administration which showed inventories down by a fraction of a percentage point for the week. The market seems to react spontaneously to changes in that crude-stocks statistic. Up is bearish, down is bullish. These days even a very modest decline in inventories is bullish. But serious analysis requires a more detailed, more nuanced understanding of why crude oil inventories behave as they do. Were inventories driven up by higher production or lower refinery runs? By higher imports? By lower exports? The reasons behind the inventory change are more important than the change itself. Today we continue our series on the modeling of U.S. crude oil supply and demand, and the sourcing of input data used in those calculations.

Wrong Road Again - U.S. E&P Earnings Resume Slide in Q2 2025 After Promising Start to Year

U.S. interstates are populated with electronic displays that update drivers in real-time on traffic conditions, road closures, weather alerts and other important events. If there was a sign for executives steering our nation’s oil and gas producers, it would likely read “Poor Visibility, Slow Down Ahead.” After a short-lived price rally in Q1 2025, the industry faced lower commodity realizations and macroeconomic headwinds in Q2 2025, which spooked investors and hardened a cautious investment approach. In today’s RBN blog, we analyze the latest results of the 39 major U.S. E&P companies we cover and look at what’s ahead.