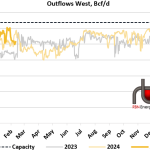

Outflows of natural gas from the Permian Basin were down slightly for the week ending February 10 compared to the week prior. Lower outflows to the West offset higher outflows to the other corridors. Outflows to the West averaged 2.56 Bcf/d, down 0.2 Bcf/d week-on-week, as can be seen in the dark orange line in the chart below. This was driven by a huge drop in outflows on El Paso towards Cornudas. Ongoing maintenance work and force majeure events on El Paso continue to cause flow disruptions, but some of those constraints may ease this spring, as the Flagstaff compressor station is expected to return to service.

Featured Articles

- Analyst Insight

Permian Natural Gas Flows Westbound Jump Back to Normal

Westbound outflows last week were up relative to the prior week, as maintenance on El Paso continues to buffet capacity.

- Blog

Already Gone - Is the Permian Basin Already Out of Natural Gas Takeaway Capacity?

After a record run of negative pricing last spring and summer, the Permian Basin collectively cheered as WhiteWater’s Matterhorn Express pipeline began flowing last October, bringing much-needed takeaway capacity to the area. Cash prices at the Waha Hub rebounded and the basin had a relatively uneventful winter, but prices began dropping in early March and have once again traded below zero for most of the past few weeks. This has taken the market somewhat by surprise, as many expected the impact of Matterhorn’s startup to last more than a few months. Prices jumped back above zero on Wednesday and above $1/MMBtu on Thursday, but with major pipeline maintenance coming next week, any relief is likely to be short lived. In today’s RBN blog, we’ll look at what’s driving the recent run of negative pricing in the Permian Basin and what it means until additional infrastructure comes online next year.

- Analyst Insight

Outbound Constraints Create Negative Waha Gas Prices for Most of Last Week

Waha natural gas prices still languished in negative territory for most of last week, as outflows were restricted on several corridors even as Matterhorn Express flowed significant volumes.