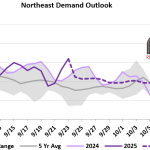

Late summer and early fall weather continue to cause a slump in regional demand for natural gas. However, the shoulder season impacts demand for gas not only in the Northeast but elsewhere. As Northeast Asian and European demand for LNG is typically low this time of year, Cove Point has scheduled its annual maintenance for this period. The LNG export facility went offline on Saturday and is expected to remain offline for roughly three weeks. Having 0.7 Bcf/d of demand disappear for that period should result in looser balances and lower cash prices for the duration.

Featured Articles

- Blog

Turn the Page - Producer Restraint, Tighter Balances Disrupt Appalachian Gas Market Trends

Before the bullish winter of 2021-22, it appeared the Northeast natural gas market was headed for familiar territory: worsening seasonal takeaway constraints and deeper, constraint-driven price discounts starting as early as this spring. Instead, the market went in the other direction the past few months. Takeaway utilization out of Appalachia has been lower year-on-year and, for the most part, Appalachian supply basin prices have followed Henry Hub higher even as that benchmark rocketed to 14-year highs. That’s not to say that constraints out of the Northeast aren’t on the horizon. But the market is now poised to escape the worst of it this year, despite the completion of the last major takeaway pipeline project in the region, Mountain Valley Pipeline (MVP), being pushed out another year or longer, if it crosses the finish line at all. In today’s RBN blog, we provide an update on regional fundamentals and what recent trends mean for gas production growth and pricing in the region.

- Analyst Insight

Appalachian Gas Production Remains High Despite Low Regional Demand

Demand for natural gas in the Northeast continued to decline, but production is holding steady in defiance of the typical shoulder-season trend.

- Blog

Hold the Line - Has the Natural Gas Market Averted an Injection Season Meltdown?

The CME/NYMEX Henry Hub prompt natural gas futures prices have been relatively rangebound this injection season and have averaged around $2.60/MMBtu since June — a third or less of where prices stood during the same period last year, in the $7-$9/MMBtu range, and at or below most natural gas producers’ breakeven costs. Yet, this is a much rosier scenario than it could have been considering that the first quarter of 2023 was one of the most bearish in over a decade and led to a massive storage surplus vs. last year that persisted through much of the summer. Since setting the year-to-date monthly average low of $2.19/MMBtu in April, prompt futures rose to an average of nearly $2.50/MMBtu in June, ~$2.65/MMBtu in July and August, and have mostly stayed in the $2.50-$2.75 range in September to date. In today’s RBN blog, we break down the factors that kept prices from unraveling this injection season to date and the implications for the rest of the shoulder season.