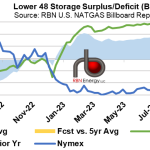

The gas market surplus in storage compared to last year could shrink to less than 500 Bcf for the first time in months in the coming weeks. After Thursday’s EIA weekly storage report, the inventory stood at 3,065 Bcf, 546 Bcf higher than the comparable storage week last year and 275 Bcf above the 5-year average. However, the temperature-based storage model suggests that the next two storage reports could show the year-on-year surplus receding by ~40 Bcf to right around 500 Bcf. Moreover, if we assume 5-year average storage activity beyond the 15-day temperature outlook, the inventory surplus could fall to the 480s Bcf by mid-September.

Featured Articles

- Blog

High Voltage - Tight Balances Supercharge Gas Market, Propel Prices Over $5/MMBtu

The natural gas futures contract for the prompt month barreled a net ~$1.00 (26%) higher in the past 12 days as the potential for prolonged production shut-ins in the Gulf of Mexico after Hurricane Ida amplified already-heightened supply fears in both the U.S. and international gas markets. The blistering price action sent the CME/NYMEX Henry Hub October futures contract soaring on Wednesday to an intraday high above $5/MMBtu and a settle of $4.914/MMBtu, the highest during September trading since 2008, while the prompt December and January contracts settled above $5/MMBtu for the first time in years. Prices at European and Asian gas/LNG hubs have similarly rallied this summer to multi-year or even all-time highs. Offshore Gulf gas production has since begun to recover, slowly, after the Ida-damaged Port Fourchon in Louisiana, the base of offshore oil and gas operations, reopened over the Labor Day weekend, but the bulk of it remains offline as power outages and other operational challenges persist. The shut-ins are exacerbating an already tight market, marked by record LNG exports, lackadaisical production growth, and a growing inventory deficit compared with year-ago and five-year average levels. Those underlying fundamentals will remain a trigger point for price spikes well after Ida-related shut-ins recover. Today, we discuss where the gas market stands heading into the final months of the injection season and the implications for winter gas pricing.

- Blog

Summertime Blues - Potential Natural Gas Storage Scenarios for the Balance of Injection Season

Hurricane Harvey has dissipated, but the affected areas, including energy infrastructure and operations, are still in recovery mode and will be for some time to come. In the natural gas market, production fell as low as 71.3 Bcf/d this past week, and has now rebounded to pre-storm levels near 72 Bcf/d. But exports to Mexico, which were averaging near 4.4 Bcf/d in the 30 days prior to Harvey, were at 3.6 Bcf/d last Friday, still lagging 0.8 Bcf/d (18%) behind their pre-storm level, after dropping to as low as 2.85 Bcf/d last week. Deliveries for LNG export are also down nearly 1.0 Bcf/d (47%) from the 30-day average to just under 1.0 Bcf/d last Friday and dropped to about 475 MMcf/d over the weekend. Meanwhile, U.S. consumption — in the power, industrial and residential and commercial sectors — this past week averaged 62.8 Bcf/d, down 6.0 Bcf/d (9%) versus last year and also 1.6 Bcf/d (3%) lower than the five-year average for this time. In another important market development, Energy Transfer Partners’ new Rover Pipeline began partial service on Friday and deliveries rose to more than 500 MMcf/d over the weekend. What will these shifts mean for the gas market balance and storage inventory? Today, we continue our analysis of the gas market balance, this time with a forward look at potential storage scenarios for the balance of injection season.

- Blog

What's Going On? - Bullish EIA Storage Report Signals a Big Shift in the U.S. Natural Gas Market

The U.S. Energy Information Administration (EIA) on Thursday (June 9) reported a surprisingly bullish 65-Bcf injection for the week ended June 3—that was 8.0 Bcf below our Natgas Billboard estimate and more than 10 Bcf below the Bloomberg industry average assessment. In response, the CME/NYMEX Henry Hub July natural gas contract screamed about 15 cents higher following the report to a settle of $2.617/MMBtu, the highest daily settle for the prompt month in nearly 9 months. Thursday’s gains extended a rally that began on May 31 (2016) just after the July contract rolled to the front of the futures curve. It’s likely the rally was initially spurred by market participants looking to cover their short positions. But in the past week, an increasingly bullish fundamental picture has emerged prompting us to raise our price outlook (in our June 10 NATGAS Billboard report). In today’s blog, we analyze the fundamentals behind rising natural gas prices.