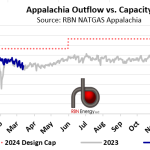

During the week ended March 12, net outflows of natural gas from the Northeast declined by an average of 0.7 Bcf/d from the previous week. This included a 0.4 Bcf/d average decline in outflows to the Southeast and Gulf Coast. Outflows to the Midwest declined 0.1 Bcf/d while net outflows to Canada fell by 0.2 Bcf/d. Total Northeast net outflows for the week averaged 14.3 Bcf/d. However, when imports from Canada are removed, total outflows from the week were 14.9 Bcf/d (blue line in chart below), which is 82% of the total outflow design capacity (dotted red line) of 18.2 Bcf/d. The previous week saw 84% of capacity in use.

Featured Articles

- Blog

Gas-Weighted E&Ps' Q2 2025 Earnings

<h3 style="margin-bottom: 0;">2nd Quarter 2025 ($in Millions)</h3><table border="0" cellpadding="0" cellspacing="0" class="tablesaw tablesaw-swipe" data-tablesaw-mode="swipe" data-tablesaw-sortable style="font-size: 10px;">

<thead>

<tr style="background-color: steelblue; color: white; font-weight"></tr></thead></table>

- Blog

Stardust, And Much More - Is There Enough Natural Gas Takeaway Capacity from the SCOOP and STACK? Part 5

Natural gas production out of Oklahoma’s SCOOP and STACK plays has been resilient in the face of lower oil and gas prices and is expected to grow by about 1.5 Bcf/d over the next five years. But with the Marcellus/Utica increasingly competing for both pipeline capacity and demand markets outside the Northeast region, the question is where can and will the new SCOOP/STACK supply go? That will be dictated in large part by where demand is growing—primarily along the Gulf Coast—and where the price differentials are attractive. But flows also can be hindered or facilitated by another, preeminent factor: pipeline takeaway capacity. Today we explore the potential for takeaway constraints out of the SCOOP and STACK.

- Analyst Insight

Northeast Gas Outflows Decline on Compressor Outage as Power Demand Up

Outflows of natural gas from the Northeast decreased last week as flows through TETCO are still down following a compressor outage.