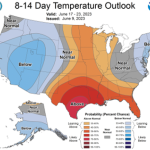

Forecasts calling for above-average temperatures drove natural gas prices higher this week, with the Henry Hub July contract settling Friday at $2.254/MMbtu, up 8.2 cents from last Friday’s close. The contract had risen every day this week before falling by 9.8 cents today as revised forecasts called for some cooling in mid-June. The National Weather Service’s 8-14 day outlook now shows below-average temps for much of the Northeast, the Rockies and the West; in earlier forecasts, temperatures were expected to be above normal across most of the U.S, with the exception of the Southwest and Rockies.

Featured Articles

- Blog

Summertime Blues - Potential Natural Gas Storage Scenarios for the Balance of Injection Season

Hurricane Harvey has dissipated, but the affected areas, including energy infrastructure and operations, are still in recovery mode and will be for some time to come. In the natural gas market, production fell as low as 71.3 Bcf/d this past week, and has now rebounded to pre-storm levels near 72 Bcf/d. But exports to Mexico, which were averaging near 4.4 Bcf/d in the 30 days prior to Harvey, were at 3.6 Bcf/d last Friday, still lagging 0.8 Bcf/d (18%) behind their pre-storm level, after dropping to as low as 2.85 Bcf/d last week. Deliveries for LNG export are also down nearly 1.0 Bcf/d (47%) from the 30-day average to just under 1.0 Bcf/d last Friday and dropped to about 475 MMcf/d over the weekend. Meanwhile, U.S. consumption — in the power, industrial and residential and commercial sectors — this past week averaged 62.8 Bcf/d, down 6.0 Bcf/d (9%) versus last year and also 1.6 Bcf/d (3%) lower than the five-year average for this time. In another important market development, Energy Transfer Partners’ new Rover Pipeline began partial service on Friday and deliveries rose to more than 500 MMcf/d over the weekend. What will these shifts mean for the gas market balance and storage inventory? Today, we continue our analysis of the gas market balance, this time with a forward look at potential storage scenarios for the balance of injection season.

- Blog

What's Going On? - Supply/Demand Factors Driving Natural Gas Price Volatility

<p>June was somewhat of a game-changer for the 2016 U.S. natural gas market. Summer weather finally arrived and U.S. consumption, particularly from power burn, was at record highs, as were exports to Mexico.</p>

- Blog

You Wreck Me - What COVID-19, Global LNG Demand Loss Could Mean for U.S. Gas Storage Refill

The U.S. natural gas market has been on edge as it awaits more clarity on the extent of the demand destruction that could transpire, both from COVID-related commercial and industrial closures and potential disruptions to U.S. LNG export activity from demand losses downstream, particularly in Europe and Asia. The CME/NYMEX Henry Hub prompt contract last week set at all-time lows for April trading — twice — before gaining ground again this week as forecasts turned decidedly more bullish for April. But the market remains under pressure, as it heads into the storage injection season with an inventory that’s well above the year-ago and five-year average levels. With the economic slowdown likely persisting, in the U.S. and globally, in the coming weeks and months, the question is, could potential demand loss send the inventory barreling toward record-high, or even capacity-testing, levels by this fall? How much demand loss would it take for that to happen? Today, we assess the potential impacts of domestic demand loss and possible LNG cargo cancellations on the U.S. gas market.