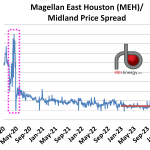

Utilizing data from RBN’s TradeView publication, the difference in the price of WTI crude oil traded at the Magellan East Houston (MEH) terminal and WTI crude oil traded at the Midland hub in the heart of the Permian Basin in West Texas, pushed to $1.41/bbl on May 1, its highest level in four years (black dashed oval in chart below). This price spread is the relative value placed on physical crude oil delivered to MEH versus crude delivered into Midland and reflects the market’s assessment of the supply and demand drivers for crude in each region. The high of May 1 was nearly four times higher than the 2024 average (Jan. 1 to Apr. 30) of $0.37/bbl (green line) and more than six times higher than the 2023 average of $0.22/bbl (red line). The MEH-Midland spread has since retreated to $1.05/bbl as of May 8, but this is still one of the highest values recorded since the market dislocations that came about at the height of COVID-related upsets in April 2020 (pink dashed rectangle).

Featured Articles

The Price is Right - North America Crude Oil Price Differentials Explain and Foretell Market Shifts

There is no debate about it: The CME/NYMEX domestic sweet (DSW) crude oil futures prompt-month contract at Cushing, OK, is the most closely followed benchmark in U.S. energy markets. It’s the price quoted in nightly news reports and general media publications. And now, with U.S. exports of WTI deliverable on the Brent contract, domestic sweet at Cushing is arguably setting the price for crudes around the world. But the fact is, most crudes traded in physical markets across North America are not priced at the DSW-at-Cushing benchmark but instead at a differential to Cushing — higher or lower on any given day based on each crude’s unique quality, location, and supply/demand characteristics. In today’s RBN blog, we discuss how the behavior of differentials from the Cushing benchmark can go a long way to explain what is happening with crude oil production, transportation volumes, storage and, of course, exports.

Glimpse of the Future - Upcoming W2W Maintenance Will Tighten Permian Oil Takeaway, Wreak Havoc on Prices

The largest crude oil pipeline exiting the Permian Basin by volume — Wink to Webster (W2W) — is planned to be offline for maintenance for the first 10 days of June. This is inclusive of Enterprise’s Midland-to-ECHO III (ME III), which reflects the company’s 29% undivided joint interest in W2W. Although the outage has not been publicly confirmed, it’s our understanding that 1.5 MMb/d of capacity will be offline to reroute a small section of pipeline. In today’s RBN blog, we’ll examine how the planned maintenance will impact Permian Basin oil takeaway capacity and what it may mean for Midland WTI pricing.