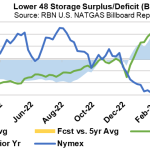

The Lower 48 natural gas storage surplus vs. last year contracted for the first time in 11 weeks. The EIA yesterday reported an above-average withdrawal of (72)-Bcf for the week ended March 17, decreasing the U.S. working gas inventory to 1,900 Bcf. The draw fell slightly short of average industry expectations but was well above last year and the five-year average for the comparable week. As a result, the surplus vs. last year decreased to +511 Bcf, from +532 Bcf previously, and the surplus vs. the 5-year inventory shrank to +373 Bcf, from +403 Bcf previously.

Featured Articles

- Blog

High Voltage - Tight Balances Supercharge Gas Market, Propel Prices Over $5/MMBtu

The natural gas futures contract for the prompt month barreled a net ~$1.00 (26%) higher in the past 12 days as the potential for prolonged production shut-ins in the Gulf of Mexico after Hurricane Ida amplified already-heightened supply fears in both the U.S. and international gas markets. The blistering price action sent the CME/NYMEX Henry Hub October futures contract soaring on Wednesday to an intraday high above $5/MMBtu and a settle of $4.914/MMBtu, the highest during September trading since 2008, while the prompt December and January contracts settled above $5/MMBtu for the first time in years. Prices at European and Asian gas/LNG hubs have similarly rallied this summer to multi-year or even all-time highs. Offshore Gulf gas production has since begun to recover, slowly, after the Ida-damaged Port Fourchon in Louisiana, the base of offshore oil and gas operations, reopened over the Labor Day weekend, but the bulk of it remains offline as power outages and other operational challenges persist. The shut-ins are exacerbating an already tight market, marked by record LNG exports, lackadaisical production growth, and a growing inventory deficit compared with year-ago and five-year average levels. Those underlying fundamentals will remain a trigger point for price spikes well after Ida-related shut-ins recover. Today, we discuss where the gas market stands heading into the final months of the injection season and the implications for winter gas pricing.

- Blog

Razor's Edge, Part 2 - Could U.S. Natural Gas Stocks Catch Up This Winter?

The U.S. natural gas market’s supply-demand balance in 2018 has been razor thin, with demand ramping up to match strong production gains. The result has been a large and stubborn storage deficit compared to prior years and price volatility, the likes of which the market hasn’t seen in a decade or more. How will the current storage level affect the winter gas market, and what are the prospects for storage to catch up before the winter is up? Today’s blog considers potential scenarios for the season-ending gas inventory balance.

- Blog

Razor's Edge - Tight Supply-Demand Balance Brings Back Natural Gas Price Volatility

Volatility is back big time in the U.S. natural gas market. The CME/NYMEX Henry Hub prompt natural gas futures contract in mid-November raced up more than $1.00 (28%) in the span of two days to a settlement of about $4.84/MMBtu on November 14, the highest price since February 2014, only to whipsaw back down 80 cents the next day. And, since then it hasn’t been unusual to see daily swings of 20-45 cents in either direction. As of yesterday, the now-prompt January 2019 contract was at about $4.34/MMBtu, down 27 cents on the day. The gas market hasn’t seen quite this level of volatility in a decade or more. Why now and what are the fundamentals behind it? With the coldest, highest-demand months still ahead, today’s blog provides an update of the gas supply-demand balance driving the recent price volatility.