It’s no secret that LNG facilities have drastically changed the landscape of U.S. natural gas markets, and business is booming. According to U.S. Census data, aggregate domestic export value of LNG was $4.7B in 2022 and $3.1B through November 2023, but there is more opportunity for LNG facilities than just exports, as illustrated by the recent bout of winter weather mid-January 2024.

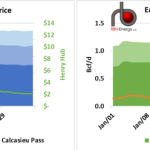

Looking at each LNG market area individually, there is a similar story to be told: winter peaks are a perk, not a problem. In Louisiana (left hand chart below), when Henry Hub spot prices peaked at around $13/MMbtu, feedgas to local LNG facilities dropped 36%. On the East Coast, (right-hand chart below) when local prices peaked near $24/MMbtu, feedgas to Cove Point and Elba Island slumped 43%, returning to near-full-utilization levels and subsequently diving back down 75%. Both cases highlight the intricacies at play between the two market areas. Louisiana’s Henry hub is geographically closer to LNG facilities, and the web of natural gas pipelines, storage facilities and market liquidity allow more opportunities for LNG offtakers to take advantage of peak prices. On the flip side, East Coast LNG offtakers are limited by both pipeline constraints and distance, as well as lack of salt-dome storage. Sure, capacity holders on the East Coast can still get their money’s worth, but have a harder time compared to facilities located within spitting-distance of the main U.S. natural gas trading hub.