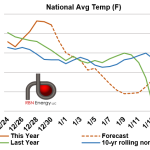

In many industries, the period between Christmas and the New Year can be the most boring time of the year with big decisions postponed until holidays have ended. However, it is frequently one of the most exciting weeks in natural gas trading, as we can clearly see this year. Gas futures have been riding high recently, as just this past Friday the January contract reached a final settlement of $3.514/MMBtu – the highest settlement for any monthly gas contract in two years. But the bulls really took over in trading on Monday, as the February contract temporarily surged above the $4.00/MMBtu mark. At one point in intraday trading, February was up 24% in its first trading day as the prompt contract, although it fell back below $4.00/MMBtu in the afternoon. Colder revisions to the weather forecast were largely responsible for the upward surge in the market. The national average temperature is now expected to be 3.4 degrees Fahrenheit below normal over the next 15 days. Our forecast (dotted brown line in chart below) shows especially cold weather during the second week of January.

Featured Articles

East is East, West is West - U.S. Natural Gas Spot Prices Race to $600/MMBtu as Midcon Runs Out of Gas

Physical natural gas spot prices in the U.S. Midcontinent trading as high as $600/MMBtu, while Northeast prices barely flinch – that was the upside-down reality physical traders were contending with Friday in trading for the long weekend, with Winter Storm Uri bearing down on large swaths of the Lower 48 and spreading bitter-cold, icy weather from the Midwest and Northeast to Texas and the Deep South. The record-shattering, triple-digit spot prices, mostly all west of the Mississippi River, were indicative of some of the worst supply shortages the market has seen during the generally oversupplied Shale Era, or ever. But the East vs. West price divergence also marks the culmination of years of shifting gas supply and flow patterns that have redefined regional dynamics. The market will be digesting the various impacts of this still-unfolding event for days, but some of the effects and implications can be gleaned already from daily pipeline flows. In today’s blog we provide an early look at the market impacts of the polar plunge.

Oops, (Winter's) Out of Time - Natural Gas Buyers Party Like It's 1999

After holding above $2/MMBtu in the first half of January, the CME/NYMEX February natural gas futures contract caved in this week, closing Tuesday and Wednesday at $1.895/MMBtu and $1.905/MMBtu, respectively. The last time we saw prices this low was in March 2016. But to see such levels trading in January, typically one of the coldest and highest-demand months of the year, you’d have to go back more than two decades — to 1999. Today, we explain the fundamentals behind the price collapse earlier this week and its implications for the 2020 gas market.

Heat of the Moment - High Gas Production, Historically Low Heating Demand Keep a Lid on Prices

So far this winter, front-month CME/NYMEX natural gas futures have fallen, risen and fallen again but, until their most recent dip, generally remained within the same $2.30-to-$3.30/MMBtu range where they have been lingering since mid-2023. With production sustaining near-record levels, LNG export volumes down from the winter highs, and temperatures back to normal, the supply of gas remains plentiful — a bearish scenario. In today’s RBN blog, we look at why there’s been a lid on natural gas prices — and the odds that the situation might change before the rapidly-approaching end of the winter season.