Featured Articles

Flirtin' with Disaster - COVID-19 Shutdowns Compound Weak Gas Demand Fundamentals

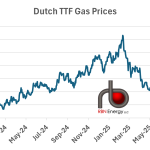

While the crude oil market meltdown has taken center stage in recent weeks, and for good reason, the natural gas market is bracing for its own fallout. The CME/NYMEX Henry Hub April futures price, which was already at a multi-year low, buckled last week, falling to as low as $1.602/MMBtu on March 23, and expired Friday at $1.634/MMBtu, the lowest April expiration settle since 1995. On its first day in prompt position, the May futures contract yesterday eked out a late-day, 1.9-cent gain that brought it back up near $1.70/MMBtu as traders continued weighing competing market factors. Gas futures earlier in March were initially buoyed by the assumption that the low oil-price environment would slow associated gas production — and it will, eventually. But that initial bullish sentiment was quickly usurped by the more immediate effects of demand losses resulting from the economic slowdown caused by COVID-19, as well as from mild weather. Today, we look at how these developments are shaping gas supply-demand fundamentals heading into the gas storage injection season.

Put Your Head on My Shoulder – Natural Gas Demand Doldrums

NYMEX natural gas prices have fallen 16 percent since reaching their high for the year so far of $4.408/MMBtu on April 19, 2013. The NYMEX August contract closed at $3.582/MMBtu on June 27, 2013.The market is currently in the low demand shoulder season. Winter is over and summer heat is on the way but temperatures in May and June are not typically high enough to significantly increase demand for air conditioning. Today we review shoulder season gas market fundamentals.

You Wreck Me - What COVID-19, Global LNG Demand Loss Could Mean for U.S. Gas Storage Refill

The U.S. natural gas market has been on edge as it awaits more clarity on the extent of the demand destruction that could transpire, both from COVID-related commercial and industrial closures and potential disruptions to U.S. LNG export activity from demand losses downstream, particularly in Europe and Asia. The CME/NYMEX Henry Hub prompt contract last week set at all-time lows for April trading — twice — before gaining ground again this week as forecasts turned decidedly more bullish for April. But the market remains under pressure, as it heads into the storage injection season with an inventory that’s well above the year-ago and five-year average levels. With the economic slowdown likely persisting, in the U.S. and globally, in the coming weeks and months, the question is, could potential demand loss send the inventory barreling toward record-high, or even capacity-testing, levels by this fall? How much demand loss would it take for that to happen? Today, we assess the potential impacts of domestic demand loss and possible LNG cargo cancellations on the U.S. gas market.