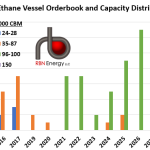

The size of ethane vessels has increased considerably in recent years, and this growth is anticipated to accelerate further with the addition of new, massive vessels to the fleet. The graphic below illustrates the historical and projected ethane vessel orderbook from the beginning of the ethane waterborne trade in 2016 through 2029. The bars represent the number of ships, in four size categories classified by thousands of cubic meters (000 CBM): small vessels (below 28 CBM), Very Large Ethane Carriers (VLECs, 35-87 CBM), larger VLECs (96-100 CBM) and the recently ordered Ultra Large Ethane Carriers (ULECs, 150 CBM).

Featured Articles

- Blog

Boats to Build – Propane Markets and the Flotilla of LPG Vessels Just Over the Horizon

U.S. production of propane from gas processing has more than doubled since 2010 and now exceeds 1.1 MMb/d. Together with another 300 Mb/d from refineries, that is far more propane than the U.S can use. Consequently, U.S. exports of propane have been booming, reaching more than 700 Mb/d in July. But that has not been enough exports to keep propane inventories from filling to the brim, now up to more than 90 million barrels, about 10 million barrels over the five year high. About the only thing that has been holding back even more exports is shipping costs. The cost of ships that move most of the propane to overseas markets, called Very Large Gas Carriers, or VLGCs (gas meaning LPG, not natural gas), have been high since U.S. exports started ramping up and then blasted to the moon this summer in response to huge export volumes and logistical tangles in global markets. But that’s all about to come to an end. There is a flotilla of new LPG vessels that were ordered many months ago that are scheduled to hit the market in 2015 and 2016. In today’s blog we review how U.S. LPG exports are likely to respond to the coming massive increase in VLGC shipping capacity.

- Blog

Stayin’ Afloat With The LP Gees – U.S. Waterborne LPG Exports 2 – Gas Carriers

Exports of liquefied petroleum gases (LPGs) from the U.S. to international markets - are expected to nearly double from 466 Mb/d in 2014 to 825 Mb/d in 2018 as production from gas plant processing exceeds domestic demand. There are two LPG export terminals on the Houston Ship Channel that have been responsible for most exports, another six around the country that have exported some LPG over the past year, and still another four new-builds that have been announced. That’s a lot of volume and a lot of dock capacity. One question is whether there are enough LPG ships to handle all of these exports. Today we introduce our review of this question, looking at the specialized vessels used to ship LPGs.

- Blog

Bottleneck Blues - Traffic at the Panama Canal and Its Impacts on LNG Economics

On the 8th of October, the LNG carrier Golar Penguin loaded a cargo for RWE at the Freeport LNG terminal in Texas. Five days later, on October 13, the vessel was sitting just north of Panama. But then, the ship abruptly changed direction on the 14th and headed towards the Cape of Good Hope to deliver to the Far East. The reason for the diversion was that the vessel did not have a passage booked in the new locks of the Panama Canal and would have had to wait approximately nine days for its turn to transit, before heading across the Pacific Ocean to Asia. Since then, as queues of LNGCs for Panama Canal transits, both northbound (ballast) and southbound (laden) have developed, more ships have opted for the longer route. In today’s blog, we look at the delays that have developed surrounding the Panama Canal and the implications that its operations hold for global LNG trade.