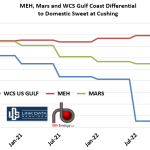

In the aftermath of the COVID crude oil price meltdown as prices recovered and then skyrocketed with the Ukraine invasion, the quality-based differentials for crudes in North America widened. As shown in the graph below, demand for light sweet crudes, represented by Magellan East Houston (MEH, 41.4 API, 0.36 % sulfur) increased relative to Domestic Sweet crude at Cushing, while the higher sulfur Louisiana offshore Mars crude delivered in Louisiana (30 API, 1.87 % sulfur) price widened, along with Western Canadian Select (21.3 API, 3.6% sulfur) traded on the Gulf Coast. But as crude oil prices declined this year, the heavy and higher sulfur crude differentials started to narrow. Note that differentials shown in the figure below are six-month averages of data provided by Link Data Services.

Featured Articles

The Price is Right - North America Crude Oil Price Differentials Explain and Foretell Market Shifts

There is no debate about it: The CME/NYMEX domestic sweet (DSW) crude oil futures prompt-month contract at Cushing, OK, is the most closely followed benchmark in U.S. energy markets. It’s the price quoted in nightly news reports and general media publications. And now, with U.S. exports of WTI deliverable on the Brent contract, domestic sweet at Cushing is arguably setting the price for crudes around the world. But the fact is, most crudes traded in physical markets across North America are not priced at the DSW-at-Cushing benchmark but instead at a differential to Cushing — higher or lower on any given day based on each crude’s unique quality, location, and supply/demand characteristics. In today’s RBN blog, we discuss how the behavior of differentials from the Cushing benchmark can go a long way to explain what is happening with crude oil production, transportation volumes, storage and, of course, exports.

Make That Connection - Understanding North American Crude Oil Markets in the Export Era

There’s a lot going on in North American crude oil markets these days. Exports are running strong. Midland WTI is now deliverable into Brent (but only if it meets specs). Pipelines from the Permian to Corpus Christi are maxed out, pushing incremental production to Houston. The price differential between WTI at Midland and Houston is nearing zero. And the value of heavy Western Canadian Select (WCS) delivered to the U.S. continues to bounce all over the place. Are these unrelated, random events in the quirky U.S. physical crude market, or are they logical developments linked by the economics of refinery preferences, quality shifts, export demand, and logistics? As you might expect, we think it’s the latter. Believe it or not, crude markets sometimes do behave rationally — and, from time to time, even predictably. That’s what we explore in today’s RBN blog.

Under Pressure - What's Shrinking the Medium and Heavy Sour Crude Discounts, and What's Next?

U.S. refiners have been enjoying some very good times the past couple of years. Most important, refining margins have soared due to a tight global product supply/demand environment brought on by, among other things, the post-COVID demand recovery, refinery shutdowns, Russia/Ukraine war effects, and high natural gas prices. Traditionally, the bulk of refining margins have come from (1) robust “crack spreads” (the general yardstick for measuring overall refining sector health, simply by taking the difference between a basket of refined products and key light sweet crude markets like WTI Cushing or MEH) and (2) the lower crude-input costs that many refineries benefit from, either because of location-related advantages or their ability to process lower-cost crude like medium and heavy sours. But location discounts have narrowed in recent years due to the buildout of pipelines and, as we discuss in today’s RBN blog, the big quality discounts that complex refiners relished through much of last year and the first few months of 2023 have withered. The question is, why?