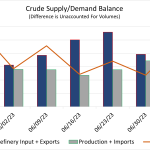

Crude oil prices had been in the doldrums for weeks, but with demand rising it seemed poised to pop given the right opportunity. That opportunity arose toward the end of last week, following bullish news of the Saudis new production cut and as U.S. domestic travel was predicted to hit a peak for the holiday weekend. The market bulls seemed eager to punish their short-selling, bearish brethren and started a rally to escape the mostly sub-$72/bbl cap it has seen in the past month. With refining demand soaring, production declining domestically, and the IEA forecating record crude demand this year, it’s no surprise that this rally has continued, as WTI closed at $77.25/bbl today. There will likely be a minor pullback soon, as usually happens following a sharp jump, but optimistic market sentiment seems to point to prices trading in a higher band than they’ve been in thus far this summer.

Featured Articles

What's Going On? - Bullish EIA Storage Report Signals a Big Shift in the U.S. Natural Gas Market

The U.S. Energy Information Administration (EIA) on Thursday (June 9) reported a surprisingly bullish 65-Bcf injection for the week ended June 3—that was 8.0 Bcf below our Natgas Billboard estimate and more than 10 Bcf below the Bloomberg industry average assessment. In response, the CME/NYMEX Henry Hub July natural gas contract screamed about 15 cents higher following the report to a settle of $2.617/MMBtu, the highest daily settle for the prompt month in nearly 9 months. Thursday’s gains extended a rally that began on May 31 (2016) just after the July contract rolled to the front of the futures curve. It’s likely the rally was initially spurred by market participants looking to cover their short positions. But in the past week, an increasingly bullish fundamental picture has emerged prompting us to raise our price outlook (in our June 10 NATGAS Billboard report). In today’s blog, we analyze the fundamentals behind rising natural gas prices.

High Voltage - Tight Balances Supercharge Gas Market, Propel Prices Over $5/MMBtu

The natural gas futures contract for the prompt month barreled a net ~$1.00 (26%) higher in the past 12 days as the potential for prolonged production shut-ins in the Gulf of Mexico after Hurricane Ida amplified already-heightened supply fears in both the U.S. and international gas markets. The blistering price action sent the CME/NYMEX Henry Hub October futures contract soaring on Wednesday to an intraday high above $5/MMBtu and a settle of $4.914/MMBtu, the highest during September trading since 2008, while the prompt December and January contracts settled above $5/MMBtu for the first time in years. Prices at European and Asian gas/LNG hubs have similarly rallied this summer to multi-year or even all-time highs. Offshore Gulf gas production has since begun to recover, slowly, after the Ida-damaged Port Fourchon in Louisiana, the base of offshore oil and gas operations, reopened over the Labor Day weekend, but the bulk of it remains offline as power outages and other operational challenges persist. The shut-ins are exacerbating an already tight market, marked by record LNG exports, lackadaisical production growth, and a growing inventory deficit compared with year-ago and five-year average levels. Those underlying fundamentals will remain a trigger point for price spikes well after Ida-related shut-ins recover. Today, we discuss where the gas market stands heading into the final months of the injection season and the implications for winter gas pricing.

What a Fool Believes - Will Crude Oil Hit $100 a Barrel?

After the crude oil price crash in the spring of 2020 and flat-at-$40/bbl oil last summer and early fall, prices for both WTI and Brent have been increasing steadily the past several months, and now stand at a kind-of-remarkable $75/bbl. This rise has been driven by a combination of demand recovery and supply restraint from both OPEC+ and U.S. producers — which begs the questions: what’s next on the supply and demand fronts, and how much more will oil prices increase from here? There’s been a lot of chatter lately that we might see $100/bbl crude prices sometime soon, and there are a lot of interested parties — many of whom don’t normally see eye-to-eye — who, for one reason or another, see their interests converge around the $100/bbl mark. The only problem is, it’s not showing up in the forward curve. Today, we look at the potential for “Benjamin-a-barrel” oil and how it might play out.