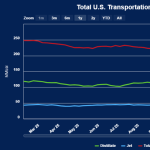

According to the EIA’s Weekly Petroleum Status Report (WPSR) released this morning for the week ended February 6, crude balances tilted bearish as rebounding U.S. production, stronger imports, and softer exports combined with lower refinery runs to drive a sizeable commercial inventory build.

As discussed in our Crude Billboard, U.S. commercial crude inventories increased by over 8.5 MMbbl to 429 MMbbl. Although this fell short of the 13.4 MMbbl build projected by the API survey results, it marks the largest weekly stock build since the same week in 2025. PADD 3 accounted for the bulk of the increase, with inventories rising by more than 5.8 MMbbl, reinforcing the view that Gulf Coast balances bore the brunt of the week’s bearish fundamentals. Smaller builds were observed across all other PADD regions. On the products side, gasoline inventories also moved higher, climbing to 259 MMbbl (far right of red line below), their highest level since May 2020, with builds seen in PADDs 1, 2, 4, and 5.