Our good friends at Turner, Mason & Company (TM&C) released the latest update to their 2012 North American Crude Oil Outlook (NACOO) today (www.turnermason.com), looking at the crude oil market from a downstream perspective – where all the light shale and heavy Canadian oil is going to go and how it is going to impact refiners when it gets there. The study is a need-to-have bible for refiners, producers and just about anyone who is trying to figure out what radical changes in the slate of available crudes, evolving quality specifications and new pricing dynamics will mean to the market over the next decade. In today’s blog “Turner Mason and the Goblet of Light & Heavy – Dumbbell Lessons Refiners Need to Learn” we review key findings from the report.

Contrary to your likely first assumption, dumbbell is not a disparaging remark directed at any particular segment of the oil industry. Instead it is a time honored reference to a specific crude oil quality issue – most would say crude quality problem. Here’s the situation. Most crude oils when they come out of the ground are relatively balanced across the yield curve. So for example, a light crude might yield 25% naphtha & lighter products, 30% middle distillates, 30% gas oils and 15% bottoms. A heavy crude will have a lot less naphtha and middle distillates and a lot more bottoms, but still the yield is spread over the different fractions. We talked more about how these fractions are processed in Complex Refining 101, Part 1 and Part 2 earlier this month.

But what if you had a crude oil with a lot of naphtha and lighter fractions, a lot of heavy bottoms and nothing in the middle? Big on one end – big on the other end. Like a dumbbell. For decades unscrupulous crude oil marketers have been buying batches of cheap heavy crude and very light crude. They then blend the two together to make a crude with API and sulfur specification that looks like West Texas Intermediate (WTI) and sell the resulting cocktail to unsuspecting refiners as WTI. Refiners hate these artificial blends because their refinery processes are balanced for real WTI, so the fake dumbbell grade throws off operations. Also because dumbbell crudes have little middle distillate fractions, the refinery produces less diesel, fuel oil and jet fuel the refined products that come from the middle distillate range. These days with diesel and related products at high prices, that’s a bad thing.

|

Check out Kyle Cooper's weekly view of natural gas markets at |

The Dumbbelling of the US Crude Slate

That gets us to one of the major findings of the TM&C report. In effect, because of the influx of a mixture of very light shale and very heavy Canadian crudes, the entire crude slate for U.S. refiners is being ‘dumbbelled’. Here’s how:

On one end, as we’ve discussed here in many RBN blogs, US domestic crude production from shale is growing rapidly. The majority of this new crude production is light sweet crude, with a significant percentage consisting of what TM&C calls Super Light crude (42 – 60 API) and for the first time in US history, large volumes of condensate – very high API gravity ultra-light liquids that are being produced from shale basins –plays like the Eagle Ford and Granite Wash. These super-lights and condensates are increasing as a percentage of the total U.S. crude mix, and are one end of our dumbbell.

The other end of the dumbbell is growing too. That is because of increasing imports of Canadian crude, which is super-heavy. We’ve talked here many times (see It's a Bitumen, oil - Does it go too far) about how very heavy crude extracted from tar sands (called bitumen) are mixed with various diluants to enable them to flow in pipelines (the resultant mix known as dilbit). In effect, dilbit is a dumbbell crude by definition.

Put these two developments together and you have a situation where the entire U.S. crude slate is starting to look more like those dumbbell crudes that the refineries don’t like – with similar consequences – Yields of middle distillates will decline, and gasoline production as a percentage of total refinery output will grow. Both of these developments are important, so let’s look a little closer at their implications.

- Gulf Coast Diesel Export Boom/Bust: For the past two years, US Gulf Coast refineries have benefited from a booming diesel export market. This is because many Gulf Coast refineries are well equipped to process conventional crudes from West Texas and the offshore Gulf of Mexico to produce high yields of the middle distillates that diesel is blended from. US refiners also have better technology to remove sulfur from the distillate pool so that they can produce diesel to ultra-low sulfur European and US specifications. These advantages together with tight international low sulfur diesel supplies have allowed Gulf Coast refineries to profit by exporting product into global markets. As the dumbbell crude mix grows as a percentage of the total crude oil supply (backing out international waterborne imports), production of diesel, fuel oil and jet fuel will fall. There just won’t be as many middle distillate molecules around. Ultimately this will wipe out much of the lucrative diesel export market.

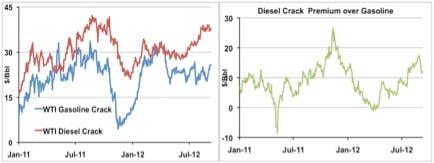

- Reduced Demand for Gasoline and Export Growth: In contrast to diesel, US domestic demand for gasoline has shrunk over the last 5 years as drivers use fuel-efficient autos and as ethanol mandate volumes replace gasoline in the tank. While gasoline exports have been growing, the international market for gasoline is more competitive than it is for diesel, so margins are lower. Chart #1 below shows the diesel crack (red line) or price spread between WTI crude and Gulf Coast diesel and the gasoline crack (price spread between Gulf Coast gasoline and WTI – blue line). (For background about crack spreads, see The Bakken Buck Starts Here). You can see that generally the refiner’s marginal return from manufacturing diesel has been higher than the marginal return from making gasoline. Chart #2 shows the spread between the two margins has averaged around $10/Bbl since the start of 2011.

Source: CME NYMEX data from Morningstar

Because of the high naphtha content of super light sweet shale crudes and the diluent component of dilbit, there will be a lot more naphtha in the U.S. crude mix, and that will make a lot more gasoline. So much more that gasoline production (as a percentage of total refinery output) will grow, resulting in the need for significant increases in gasoline exports. Pressure to export gasoline will be a good thing for lower gasoline prices here in the U.S.

Other Topics and Conclusions from the TM&C Study

We’ve focused so far on the dumbbelling issue, but the TM&C study is 100+ pages, includes a lot more numerical supplements, and covers many more topics including implications of the change in crude oil supplies on refineries and refined product markets. We’ll bullet out some of the key findings here:

- Midwest Infrastructure Logjam and Pricing Impacts: Increased crude production in North Dakota and increased imports of Canadian crude have accumulated a growing stockpile of crude in the Midwest at the Cushing storage hub. More crude is being produced than can be consumed by Midwest refiners and the infrastructure to carry this crude to the Gulf Coast where sufficient refining capacity is located, has yet to be built out. The study provides details about various pipeline projects that will eventually rectify this situation, how the different projects will impact regional prices as they come on, and examines the ultimate implications of the relationship between the global crude oil price level and crude prices in North America. The study explains how and why Light Louisiana Sweet (LLS) will trade at a discount to Brent and describes the ramifications for many other grades of crude oil.

- Growing Supplies of Light Sweet Crude Will Reduce Refining Capacity: Many U.S. refiners simply do not have the capacity to run lighter-than-planned shale crudes. Their refineries are not configured to process increasing quantities of light crudes due to column limitations, compressor constraints, overhead cooling issues and other problems – all of which can limit charge rates. Put simply, that means the refinery process overflows because the crude produces more light products than the units were built to handle. The only way to counteract this short term is to reduce the throughput volume. As a result, U.S. refinery capacity will decline by the equivalent of 2 or 3 average refineries during the 2013-17 timeframe unless compensating investments are made.

- Lower Overall Crude Pricing: Already crude supplies from Canada, North Dakota and Texas are being delivered to Gulf Coast refineries by rail and pipeline, impacting crude pricing. As new pipeline infrastructure allows growing North American supplies to reach the Gulf Coast, these supplies will exert downward pressure on crude prices. U.S. refiners will enjoy a feedstock price advantage relative to most of the world, increasing their opportunities for exports. Although Midcontinent and Gulf Coast refiners will reap most of the benefits of the increasing supplies through reduced feedstock costs, even East and West Coast refiners will gain access to new crudes and improve their economics.

- Feedstock Trading Opportunities: All of these changes in the mix of crude oils being run at refineries will result in imbalances of various intermediate feedstock streams within the U.S. refining system. Some will produce excess volumes of light intermediate streams like reformer feed and light straight run. Others will be short of some of the heavier intermediate streams, such as FCCU feed. (See Complex Refining 101, Part 1 and Part 2). The only way for these supplies to get balanced out will be through trading the intermediate streams between refineries. This will result in lucrative trading opportunities to match refinery feedstock surpluses and shortages around the country.

There are clearly a lot more details in the TM&C study than we have time to go into here. These include case studies of different refinery configurations around the U.S., tabulations of refinery projects, forecasts of geographic and quality differentials for the major grades of crude oil, and what you would expect – price and production forecasts for all the major grades of crude oil.

Surging US and Canadian crude production threatened to hit the wall earlier this year as midstream companies struggled to find paths to deliver the new crude to market. Finally the pipeline projects are underway and the crudes are finding their way to refineries by hook or by rail. Now the spotlight turns to US refiners. They face a whole new set of challenges from a dumbbell slate of crudes to changing market demand for gasoline and distillates, and rapidly evolving crude oil pricing relationships. As we are confident Dumbledoor would tell Harry Potter – time spent in the library today with studies like Turner and Mason’s NACOO, will spare savvy refiners tears in the field tomorrow.

Comments

Great blog as usual! Question on refineries though. We all know that the gulf coast refineries spent lots of time and money reconfiguring to run heavy crudes and with the resurgence of light sweet crudes. However, my question is would these same refineries consider reconfiguring once again (or at least increase optionality) to run the lighter crudes and add gasoline export capacity? I've heard that it's not too terribly capital intensive to reconfigure, but I'm not 100% certain on that. Seems like the U.S. is well positioned to feed gasoline to emerging markets in south america, much like what the propane market is doing currently.

Great blog as usual! Question on refineries though. We all know that the gulf coast refineries spent lots of time and money reconfiguring to run heavy crudes and with the resurgence of light sweet crudes. However, my question is would these same refineries consider reconfiguring once again (or at least increase optionality) to run the lighter crudes and add gasoline export capacity? I've heard that it's not too terribly capital intensive to reconfigure, but I'm not 100% certain on that. Seems like the U.S. is well positioned to feed gasoline to emerging markets in south america, much like what the propane market is doing currently.

In reply to the future of North American refining capacity by Mark Chung

Thanks for the question - which kind of hits the nail on the head as far as refiners are concerned. It is certainly possible for them to reconfigure again to process lighter crudes but that would not be an overnight process and would require significant investment. In the longer term this is likely to happen as they adjust to the new supply situation. The fact that the upgrades to handle heavy crude are just now coming to fruition gives an idea of how long these changes take. I do not have any feel for the relative costs of such changes.