Western Canadian producers regularly have to swallow large price discounts for heavy crude versus the US benchmark West Texas Intermediate (WTI). During the first week of November price discounts for heavy Western Canadian Select crude versus WTI came close to $42/Bbl – the deepest since 2007. Since then they have narrowed but are still over $30/Bbl. Today we examine the relationship between storage volumes in Alberta and crude price discounts.

This is Part 2 of our series on Canadian crude oil storage. In Part 1 we looked at increasing Canadian crude oil production and expanding pipeline capacity in the two crude marketing hubs of Edmonton and Hardisty. The two hubs are the staging posts for crude oil exports to the US as well as the distribution point for diluent supplies coming into the oil sands production region. Today we turn our attention to the relationship between Canadian crude pricing, congestion on the crude pipelines leaving Edmonton and Hardisty, and storage inventory.

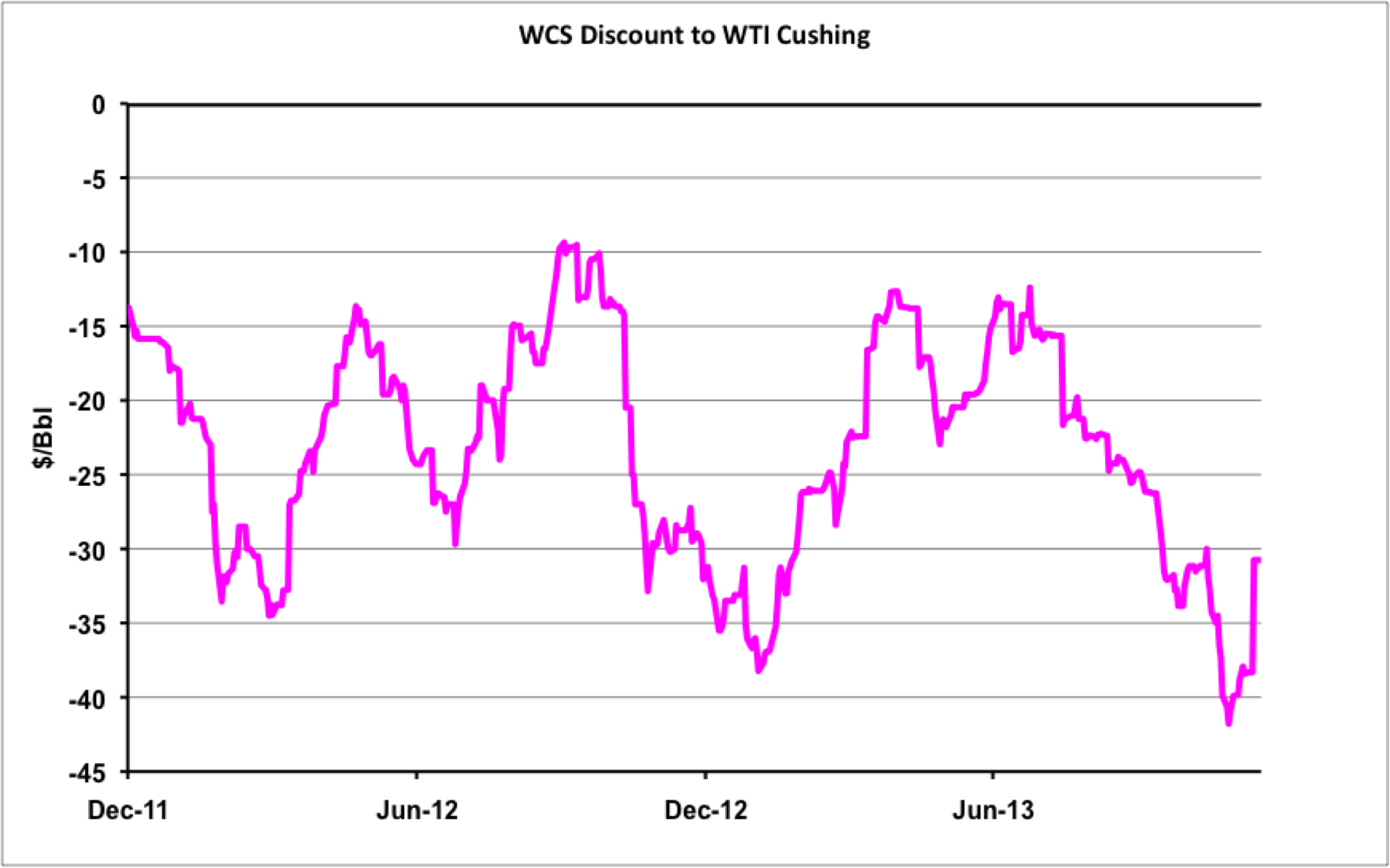

The chart below shows the price discount between oil sands benchmark Western Canadian Select (WCS) crude priced at Hardisty and the US benchmark West Texas Intermediate (WTI) at Cushing OK. On November 5, 2013 the WCS discount to WTI at Cushing reached close to $42/Bbl – its widest level since 2007. The WCS discount has averaged $23/Bbl over the past two years and $24/Bbl so far this year. The two crudes have different qualities – WCS is a heavy sour crude blend made with diluent (see It’s a Bitumen Oil – Does it Go Too Far?) and WTI is a light sweet crude that is less complicated to refine and therefore more valuable. But the WCS price discounts to WTI experienced at Hardisty are far wider than the quality differential warrants. In fact the discounts have been mainly caused by congestion on the pipeline systems out of Canada to the US or further downstream in the US Midwest from Chicago to Cushing, OK. The congestion requires Canadian producers to compete for pipeline capacity to ship their crudes to US refiners and as a result they have frequently had to accept heavily discounted prices.

Source: CME Data from Morningstar

The pipeline congestion primarily results from insufficient pipeline capacity being available to carry Canadian production looking to reach US market destinations. This lack of capacity compared to shipper nominations results in pipeline operators apportioning the space made available to committed shippers – cutting their nominated volumes by a percentage to accommodate everyone. At times the congestion gets worse (as it did in early November) when pipeline operators perform maintenance that restricts capacity further. For example, Enbridge – the operator of the 2.5 MMb/d mainline from Edmonton to Superior, WS apportioned the “Line 4” pipeline on the system in November by 13 percent. The congestion on pipelines out of Canada has been further exacerbated by growing volumes of North Dakota Bakken crude production vying for the same routes to reach markets in the Midwest and ultimately the Gulf Coast. Delays in the permitting and approval of new pipeline projects to increase capacity between Canada and the US such as the Keystone XL pipeline have added insult to injury.

Continued congestion on the pipelines out of Canada leaves producers little option but to take the discounted prices on offer or to put their crude into storage at Edmonton or Hardisty in the hope of better prices in the future. In the past year a third option has developed that is just now becoming feasible as operators complete infrastructure build out – and that is using crude-by-rail transport to bypass the congestion.

And so, in response to the demand from crude producers looking to hold their supplies in Canada until US prices improve, significant storage capacity has been built out in Hardisty and Edmonton and continues to expand. There is no official data that we are aware of on the actual storage capacity in tanks at Hardisty and Edmonton. However, the best commercial information available comes from our friends at Genscape who maintain a weekly database of the storage levels at both Hardisty and Edmonton. Genscape estimate total current crude storage capacity at Edmonton to be around 12.5 MMBbl in above ground tanks. Storage capacity at Hardisty is currently 18.6 MMBbl in above ground tanks plus 3 MMBbl of underground salt cavern storage owned by Enbridge.

Comments

Add Freight+Storage WCS-WTI discount is Gone and then it looks like that canadian shippers are playing a contango between Hardisty, Ab and Cushing,Ok.

Simon

The discount for Canadian WCS from the price of WTI is a compound of two discounts one for location but also one for quality. " WCS is a heavy sour crude blend made with diluent" as the author states and WTI is light and sweet. A more transparent indication of the role of transportation constraints on the value of WCS would have been made if the author had the author comparted the price of WCS with a waterborne crude of comparable quality such as those exported by Mexico and Venezuala.

In reply to Discounts for WCS by Levis Kochin

Hi Buddy,

You are technically correct that a straight comparison of WCS and WTI is not accurate. However, the discounts experienced for WCS at Hardisty are clearly more than just quality related and it is the "congestion" element that I wanted to highlight. The market watches WTI because it is the most transparent price - so the WCS-WTI spread is psychologically significant for Canadian producers.

Sandy

"A more transparent indication of the role of transportation constraints on the value of WCS would have been made if the author had the author comparted the price of WCS with a waterborne crude of comparable quality such as those exported by Mexico and Venezuala."

Not sure about this statement.

Here's why:

Regarding the Maya-22 and WCS.

Although Maya-22 and WCS share some similarities (mainly API and S content)

They are still two different commodites.

* Pemex's Mayas output has peaked in 2004, the log linear (%) production is steady declining for Maya-22 since a decade meanwhile the WCS output is just the exact opposite.

* At the same time bitumen production is increasing at a faster (%) than WCS because of a lack of upgraders, hydro-cracking, hydro-treating, bottlenecking. The resulting surplus in bitumen production is at discount to WTI at which dilbit(diluants+ bitumen) currently sells.

* ex-Cushing crude assessment is still different from assessed Maya-22 prices.

Mexico uses quite a complex formula in pricing its exports to the US which includes a weighted average of the prices of West Texas Sour (WTS), Louisiana Light

Sweet (LLS), Dated Brent, and High Sulfur Fuel Oil (HSFO). which looks like [(0.4 * ( West Texas Sour + 3% HSFO)) + (0.1 * (LLS + Dated Brent))] + Adjustment factor.

WCS is priced with the WTI, against very different prices assessments.

The result is that the MAYA22-WCS is the spread that is showing the utmost level of randomness: 5$, 24.26$ 11.36$ since 2 years.

By intuition, each leg of the spread has a different underlying benchmark; they are arguably totally different even if they look like two apples. I will also point out three things that Maya22-WCS has;

* even volatility skew.

* the 2 prices series (legs) within this spread aren't co-integrated. (stat metric)

*Maya is waterborne crude, WCS isn't. Not a single drop of U.S Origin crude grades commingled with WCS can be exported from US in a vessel.

(vii) Exports of foreign origin crude oil where, based on written documentation satisfactory to BIS, the exporter can demonstrate that the oil is not of U.S. origin and has not been commingled with oil of U.S. origin. See paragraph (h) of this section for the provisions of License Exception SPR permitting exports of certain crude oil from the Strategic Petroleum Reserve.

15 C.F.R. § 754.2WCS-WTI spread despite grade differential, is still relevant economically. Like Sandy said: The market watches WTI because it is the most transparent price - so the WCS-WTI spread is psychologically significant for Canadian producers.

Refineries configurations are not random and have a heavy pricing, they are the one who set and impact the H/L spreads. If there is a supply glut of light oil from Bakken it is actually good for the Heavy.

PADD II Downstream refinery such Flint Hills Resources Pine Bend have the set-up to crack the albertan bitumen into lighter products so catch most of the spread, they will continue to do it even if they can source higher quality raw supply from the bakken shale. They can make 600% more money with Albertan Heavy Grades than processing the WTI or at premium priced crudes.

Most of the Heavy Cracking capacity is in the USGC. If you have read RBN blog last month, you may have noticed that many of these cracking units where shut down for planned maintenance. This is another factor moving move WCS-WTI violently up and down.

Simon

http://jacquessimon506.wordpress.com/