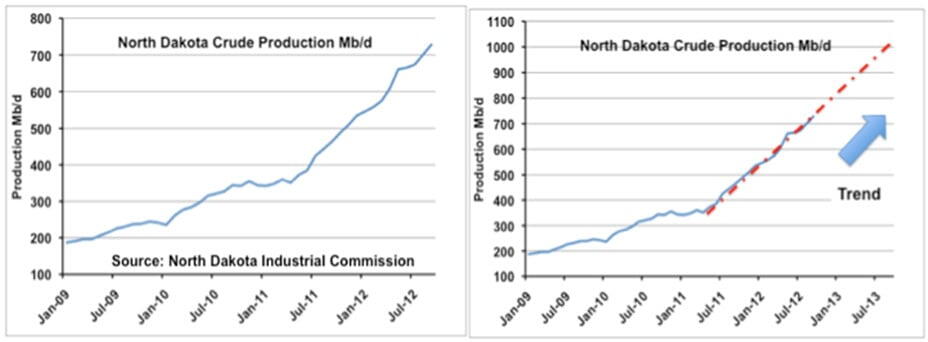

Last week the latest set of Bakken crude production numbers showed another big increase to reach 728 Mb/d. The challenge all along for this prolific land locked basin has been one of finding a ready market for growing production. Meeting that challenge in the absence of quickly available pipeline capacity led to creative solutions and many new destinations. Today we contemplate what they are going to do with all that crude.

This new record production level for September 2012 is up another 27 Mb/d over August. North Dakota now accounts for nearly 12 percent of total U.S. crude production, up from 1 percent less than five years ago. RBN Energy blog readers will be familiar with the reasons behind these production statistics. We recently covered overall US production increases from shale oil in the big three plays – the Bakken, Permian and Eagle Ford basins (see Will the Crude Production Boom Keep Running?). The charts below show the pace of Bakken crude production since the start of 2008. [The data is for North Dakota but remember that there is also Bakken production in Montana (~50 Mb/d) and South Dakota (~5Mb/d)]. The chart on the left shows actual monthly production in Mb/d. We added a trend projection (red dotted line) to the same chart on the right – following the period of most rapid growth from July 2011 and projecting forward until production hit 1 MMb/d during the 4th quarter of 2013.

Comments

The one monkeywrench in all this is that 2012 has been an exceptionally good year for shipping by rail, as a tremendous amount of coal-fired electric generating capacity was idled by low gas prices. Futures prices are already showing us what next year will look like - less coal-to-gas switching, and a possible resumption of coal shipments out of the Powder River basin as coal again becomes competetive with gas for most power producers. And since coal can account for as much as half the rail traffic in this country, that'll be a lot of cars back on the rails competing with tanker cars coming out of more or less the same region, and going to more or less the same destinations (West Coast excluded). Shipping costs will go up again, and track availability may simply not be there anymore.

While pipelines may not offer Bakken producers that flexibility shipping by rail does, they do have one advantage - nobody ships coal through them.

Thank you as always for the terrific analysis.