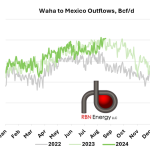

The negative cash price at Waha has been a persistent theme in the gas market this year, as more than 42% of all trading days so far in 2024 have averaged a negative price according to Natural Gas Intelligence (NGI) data. August has contributed to that large share, as Waha has traded in negative territory every day this month. However, the price averaged negative $1.58/MMBtu over the past week, which was $0.48/MMBtu higher than the price for the week ended August 12. The upward price movement coincided with ouflows from the Permian increasing by 40 MMcf/d week-on-week.

Featured Articles

- Analyst Insight

Ascent of Matterhorn Causes Waha Gas Prices to Climb

Measurable flows of natural gas began on Matterhorn at the beginning of this month. Although not as long in the making as the Karl Marlantes novel of the same name, Matterhorn has been hotly anticipated this year and will greatly impact gas flows and basis prices in Texas.

- Blog

Summertime Sadness - Is the Rangebound Summer Gas Market Heading for a Breakout?

The summer of 2024 proved somewhat melancholy for natural gas bulls, but also for bears, as front-month futures have consistently sported a $2 handle on the vast majority of trading days. What happened to the dire predictions of oversupply heard this past winter? And what about the bullish swing that took over the market in early June? Developments in production and weather have ameliorated both concerns but new issues may cause volatility to return in the near future. In today’s RBN blog, we’ll detail what happened during this summer’s gas market and what current trends portend for the fall and winter.

- Blog

Already Gone - Is the Permian Basin Already Out of Natural Gas Takeaway Capacity?

After a record run of negative pricing last spring and summer, the Permian Basin collectively cheered as WhiteWater’s Matterhorn Express pipeline began flowing last October, bringing much-needed takeaway capacity to the area. Cash prices at the Waha Hub rebounded and the basin had a relatively uneventful winter, but prices began dropping in early March and have once again traded below zero for most of the past few weeks. This has taken the market somewhat by surprise, as many expected the impact of Matterhorn’s startup to last more than a few months. Prices jumped back above zero on Wednesday and above $1/MMBtu on Thursday, but with major pipeline maintenance coming next week, any relief is likely to be short lived. In today’s RBN blog, we’ll look at what’s driving the recent run of negative pricing in the Permian Basin and what it means until additional infrastructure comes online next year.