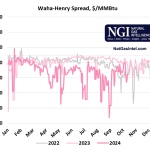

For much of this year, Waha cash prices have languished in negative territory as high production in the Permian Basin ran up against insufficient outflow capacity. The news that Matterhorn Express was online raised the prospect that negative prices would end as the pipeline ramped up to an additional 2.5 Bcf/d in flows to markets in the East. In the first week of October this seemed to be happening, as outright cash prices at Waha surged to their highest level since January only a few days after the first flow data from Matterhorn became available. However, this trend reversed sharply last week. Overall outflows from the Permian were up 0.22 Bcf/d week-on-week, primarily driven by higher outflows on the East Corridor with flows ramping up on Matterhorn. Outflows to the East averaged 11.14 Bcf/d, up 0.44 Bcf/d week-on-week. Matterhorn Express itself does not have to report pipeline flows because it’s an intrastate pipeline, but some flow data for the pipe is reported through connections with interstate pipelines. Flow data indicates the pipeline began service on October 1, although potentially some segments started earlier than that. The pipeline has been delivering about 0.45 Bcf/d to Transco Pipeline in Wharton County, Texas and between 0.1 Bcf/d and 0.23 Bcf/d to Texas Eastern Pipeline in Austin County, Texas.

Featured Articles

Ascent of Matterhorn Causes Waha Gas Prices to Climb

Already Gone - Is the Permian Basin Already Out of Natural Gas Takeaway Capacity?

After a record run of negative pricing last spring and summer, the Permian Basin collectively cheered as WhiteWater’s Matterhorn Express pipeline began flowing last October, bringing much-needed takeaway capacity to the area. Cash prices at the Waha Hub rebounded and the basin had a relatively uneventful winter, but prices began dropping in early March and have once again traded below zero for most of the past few weeks. This has taken the market somewhat by surprise, as many expected the impact of Matterhorn’s startup to last more than a few months. Prices jumped back above zero on Wednesday and above $1/MMBtu on Thursday, but with major pipeline maintenance coming next week, any relief is likely to be short lived. In today’s RBN blog, we’ll look at what’s driving the recent run of negative pricing in the Permian Basin and what it means until additional infrastructure comes online next year.