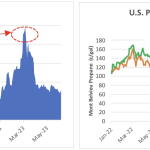

Profit margins were pretty good for U.S. propane dehydrogenation (PDH) plant operators in 1Q23. As show on the left-hand chart below, PDH propylene margins peaked at almost 50 c/lb in early March as polymer grade propylene prices (PGP) soared to over 70 c/lb. However, the party didn’t last long as margins tanked in 2Q23 and currently sit at about 14 c/lb. So, what happened to those juicy profit margins earlier in the year? PDH plant profitability is primarily determined by the difference between the cost of the propane purchased and the price of the propylene sold (the ‘‘propane-to-propylene spread’’). The wider the price differential between propane and propylene, the larger the PDH plant gross profit margin. The right-hand chart below shows the steep decline in the propylene-to-propane spread since March as PGP prices have plunged to around 30 c/lb. And you certainly can’t blame the margin decline on feedstock costs as propane prices have also been weak currently trading at only about 35% of WTI crude oil.

Featured Articles

Stop Draggin' My Heart Around - On-Purpose Propylene Doesn't Come Easy

Fast-rising NGL supplies during the early years of the Shale Era fueled excitement about the potential for new petrochemical plants in the U.S., especially ethane-only crackers to make ethylene and other byproducts, along with propane dehydrogenation (PDH) plants to make propylene. While 11 new ethane-fed crackers have come online in the U.S. since the mid-2010s and the world’s largest — Chevron Phillips Chemical and QatarEnergy’s 4.8-billion-lb/year facility — is under construction in Texas, only three of the many PDH projects proposed over the same period were actually built. In today’s RBN blog, we’ll look at why the initial rush of new PDH project announcements resulted in so few new U.S. plants.

U.S. Propylene Margins Remain Under Pressure As Propane Prices Rally

Son of a PDH Man? – Six New North American Propylene Plants On The Way

Between 2015 and 2018 five new U.S. propane dehydrogenation (PDH) plants are expected online – producing over 9 billion pounds a year of propylene. Williams are building another new PDH plant in western Canada. Five of these plants will be located on the Texas Gulf Coast – the center of the world’s chemical industry. Once they are up and running they should have a profound impact on U.S. and international markets for propane and propylene. Today we describe plans to develop these new plants.