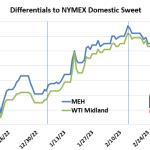

From early January 2023 to mid-February, all sweet crude differentials versus NYMEX domestic sweet (NYMEX DS) increased significantly. As shown in the graphic below, the Houston benchmark Magellan East Houston (MEH) moved up from about $0.50/bbl to $2.85/bbl by February 14, while WTI Midland moved from $0.25/bbl to $2.60/bbl over the same timeframe. But at that point the differentials changed direction, falling back significantly. On Friday MEH averaged $1.10/bbl while WTI Midland was at $0.70/bbl.

Featured Articles

- Blog

The Price is Right - North America Crude Oil Price Differentials Explain and Foretell Market Shifts

There is no debate about it: The CME/NYMEX domestic sweet (DSW) crude oil futures prompt-month contract at Cushing, OK, is the most closely followed benchmark in U.S. energy markets. It’s the price quoted in nightly news reports and general media publications. And now, with U.S. exports of WTI deliverable on the Brent contract, domestic sweet at Cushing is arguably setting the price for crudes around the world. But the fact is, most crudes traded in physical markets across North America are not priced at the DSW-at-Cushing benchmark but instead at a differential to Cushing — higher or lower on any given day based on each crude’s unique quality, location, and supply/demand characteristics. In today’s RBN blog, we discuss how the behavior of differentials from the Cushing benchmark can go a long way to explain what is happening with crude oil production, transportation volumes, storage and, of course, exports.

- Blog

Trading in the USA, Encore Edition - Pulling Back the Curtain on North America's Crude Oil Trading Market

Trading in the highly integrated US/Canadian crude oil market is undergoing a profound transformation, driven mostly by the pull of exports off the Gulf Coast. But the shifts in flows, values and even the trade structures being used today are not well understood outside a small cadre of professional traders and marketers. Consider a few examples: Domestic sweet oil traded at Cushing on NYMEX is not West Texas Intermediate — WTI at Cushing has averaged a hefty $1.80/bbl over NYMEX for the past year. Most spot Houston and Midland crudes trade as buy-sell swaps. WTI in Houston trades at a discount to Corpus Christi and sweet crudes in Louisiana. Crude in Wyoming trades at a premium to Cushing. And the Gulf Coast is the highest-value market for Canadian heavy crude. This is not your father’s (or mother’s) oil trading game. Our mission in this blog series is to pull back the curtain on physical crude trading in North America, explain how it works, what sets the price, and who is doing the deals.

- Blog

Trading in the USA - Pulling Back the Curtain on North America's Crude Oil Trading Market

Trading in the highly integrated US/Canadian crude oil market is undergoing a profound transformation, driven mostly by the pull of exports off the Gulf Coast. But the shifts in flows, values and even the trade structures being used today are not well understood outside a small cadre of professional traders and marketers. Consider a few examples: Domestic sweet oil traded at Cushing on NYMEX is not West Texas Intermediate — WTI at Cushing has averaged a hefty $1.80/bbl over NYMEX for the past year. Most spot Houston and Midland crudes trade as buy-sell swaps. WTI in Houston trades at a discount to Corpus Christi and sweet crudes in Louisiana. Crude in Wyoming trades at a premium to Cushing. And the Gulf Coast is the highest-value market for Canadian heavy crude. This is not your father’s (or mother’s) oil trading game. Our mission in this blog series is to pull back the curtain on physical crude trading in North America, explain how it works, what sets the price, and who is doing the deals.