Lately, we have noticed a lot of mention of 2022 well results along with a narrative that production per lateral foot was down versus the prior year. These “disappointing” performances coupled with depleted inventories of drill spots are cited as reasons for lackluster production growth and the need for acreage consolidation. We tackled the issue of reserves in an Analyst Insight earlier this week (see Say You’ll Be There) and today we turn our attention to the well performances. We will say, right off the bat, that we have verified lower crude oil initial production rates for each Permian sub-basin in 2022 versus 2021 based on data from Enverus. So, is the end nigh or might there be other explanations to mitigate the declines quoted in the press?

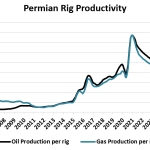

As you might expect, when you put the lower performance in context, it changes the story. So we’ve got to start by recalling what happened as a result of the 2020 Covid crash. Lockdown measures hammered demand which caused prices to tumble followed by producer activity and then production. With the pace of new well completions slowed to a crawl, rig productivity measured by the EIA initially tumbled. But as prices slowly recovered, producers tried to dig themselves out by leaning on previously drilled but uncompleted (DUC) wells in their best acreage to foster the best economic returns possible. As demonstrated by the graph of Permian rig productivity, below, this caused rig productivity to temporarily soar, followed by a reversion to the previous trend over the course of 2021 and 2022.