The record streak of negative Permian Basin natural gas prices has come to a close according to data from Natural Gas Intelligence (NGI). Waha recorded negative cash prices every day between March 12 and March 28 – a total of 17 gas days. This surpasses the previous record of 14 days where producers had to pay to have their gas taken away, which was recorded in the spring of 2019. Over the past week outright Waha cash prices have averaged -$0.06/MMBtu which is up $0.53/MMBtu week-on-week. During trading on Thursday for the long Easter weekend, the Waha cash price jumped to $0.085/MMBtu, which ended the negative streak.

Featured Articles

- Blog

Don't Blame Me - What's Causing Negative Gas Prices in the Permian and How Long Will They Last?

Natural gas prices at the Waha Hub in West Texas have been below zero for going on two weeks — that’s outright negative cash prices, not basis, which means Permian producers are literally paying to have their gas taken away. Ample supply along with weak demand have prompted an early start to the injection season this year and are putting downward pressure on U.S. gas prices more broadly. But why all the craziness now? One of the best ways to get a handle on the Permian gas-market meshugah is to examine gas pipeline flows within the basin and without, which, as it turns out, is the focus of our upcoming School of Energy Master Class. Today's RBN blog is a blatant advertorial for that event where we’ll be discussing gas-flow analysis, pipeline modeling and how they help explain why Waha gas prices have gone sub-zero.

- Analyst Insight

Free Gas and Free Money in the Permian Basin

Natural gas prices at Waha have been negative for two weeks according to data from NGI. Lack of exit capacity has played a major role in exacerbating the price situation, with probable maintenance events affecting both eastbound and westbound flows.

- Blog

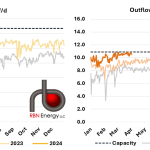

Already Gone - Is the Permian Basin Already Out of Natural Gas Takeaway Capacity?

After a record run of negative pricing last spring and summer, the Permian Basin collectively cheered as WhiteWater’s Matterhorn Express pipeline began flowing last October, bringing much-needed takeaway capacity to the area. Cash prices at the Waha Hub rebounded and the basin had a relatively uneventful winter, but prices began dropping in early March and have once again traded below zero for most of the past few weeks. This has taken the market somewhat by surprise, as many expected the impact of Matterhorn’s startup to last more than a few months. Prices jumped back above zero on Wednesday and above $1/MMBtu on Thursday, but with major pipeline maintenance coming next week, any relief is likely to be short lived. In today’s RBN blog, we’ll look at what’s driving the recent run of negative pricing in the Permian Basin and what it means until additional infrastructure comes online next year.