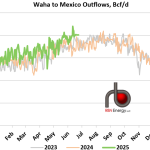

Waha natural gas cash prices increased last week, buoyed by an increase in outflows from the region, specifically to the North and East. Outflows to the North averaged 1.92 Bcf/d, up 0.15 Bcf/d week-on-week, driven by rebounding outflows on El Paso, on the route towards the Midcontinent. Meanwhile, outflows to Mexico averaged 2.01 Bcf/d, down 0.04 Bcf/d week-on-week. Outflows to Mexico have been very strong this June, flows are currently in line with previous years’ peak levels already this summer, as seen in the chart below.

Featured Articles

- Analyst Insight

Waha Gas Prices Back to Positive as Mexico Exports Remain High

Exports to Mexico have been near their maximum achieved levels recently, as Waha gas prices recover despite Westbound outages on El Paso.

- Blog

Headed for Heartbreak, Part 4 - Will Northeast Gas Outflows to the Gulf/Southeast Max Out Capacity This Spring?

Natural gas pipeline takeaway constraints out of the Northeast worsened in 2020 despite producer cutbacks in the region as high storage levels and weaker demand led to record volumes of Appalachian gas supplies needing to find outlets in other regions last fall. This year, storage levels are lower and could absorb more of the surpluses during injection season. However, Appalachian gas production so far in 2021 has been averaging higher than last year; and, gas prices are higher year-on-year, reducing prospects for the kinds of producer curtailments we saw last year. As for the “pull” from downstream demand, LNG exports along the Gulf Coast aren’t expected to experience the slump from cargo cancellations seen last summer. In other words, Appalachia’s outbound flows are likely to be robust, setting the stage for takeaway constraints and weak prices, particularly during the spring and fall shoulder seasons. How much outbound capacity currently exists and how much room is there for growth? Today, we continue our series on the Northeast gas market with an update on Appalachia’s southbound takeaway capacity and outflows, starting with a detailed look at the gas moving to the Southeast and to the Gulf Coast.

- Analyst Insight

Gas Outflows to Mexico High on Strong Permian Production

Natural gas outflows from the Permian Basin to Mexico are back at seasonal highs, boosted by high Mexican demand and high production.