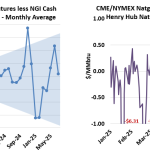

The differential between the front-month CME/NYMEX Henry Hub futures contract and the NGI daily cash price at Henry Hub has grown significantly more volatile over the past 2.5 years. As shown in the left-hand graph below, the average monthly differential in 2023 was just $0.12/MMBtu, ranging from a high of $0.33/MMBtu to a low of $0.02/MMBtu. However, that spread surged to $0.94/MMBtu in November 2024, swung down to $-0.44/MMBtu in January-February 2025, and climbed back to average $0.94/MMBtu in June 2025.

Featured Articles

- Blog

2023 Gas-Weighted E&Ps' Financial Results

<p>(Note: Each column is sortable by clicking once or twice on the column title. For example, clicking on "Revenue" will rank the companies either low-to-high or high-to-low.)</p>

- Blog

Un-Thinkable - Is the Market Ready for 100-Bcf/d U.S. Natural Gas Production?

The once unthinkable level of 100 Bcf/d for U.S. natural gas production is just around the corner, it would seem. Lower-48 gas production last week hit a new high of 96.4 Bcf/d, after surpassing 95 Bcf/d not too long ago (in late October). That’s remarkable considering that production was only 52 Bcf/d just 12 years ago. Gas demand from domestic consumption and exports this year has set plenty of records of its own, but the incremental demand has not been nearly enough to keep the storage inventory from building a significant surplus compared with last year. CME/NYMEX Henry Hub prompt gas futures prices tumbled nearly 40 cents last week to $2.28/MMBtu, the lowest November-traded settle since 2015. Today, we break down the supply-demand fundamentals behind this year’s bearish storage and price reality.

- Blog

Living in Fast Forward Curves – Making Sense of Forward Natural Gas Markets

Six months ago, the natural gas forward price for 2021 averaged $5.15/MMBtu. Back then a producer could hedge forward production at that price. Today 2021 is only $4.63/MMBtu, a decline of $0.52/MMBtu even though we are now in the middle of the winter. Today the forward market doesn’t get above $5.00/MMBtu until 2026, certainly a disappointment for many a producer that didn’t hedge last summer. What does the market know about the future that is different from what was known back in June? How do these forward curves work in the first place? In this new blog series on North American natural gas forward curves we will provide background on the mechanics of forward curves, examine the forward curve in each of the major regions in the North American natural gas market, and do a deep dive into natural gas historical trends, major drivers and market expectations as related to forward markets.

Comments

Should the marketplace not want to view this spread as the next day cash prices (the most liquid ultra prompt) minus full month ahead futures?