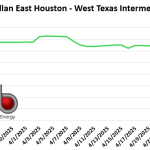

Last week marked the expiration of the May WTI contract at $64.31/bbl April 22, and the conclusion of the May pipeline shipping cycle three days later April 25. Within this three-day period, downward pricing pressure was seen across a variety of crude grades, as discussed in this week’sTradeview Report. With the commencement of new pipeline cycles, traders have a couple of options if they do not want to be responsible for physically delivering or receiving barrels: they can roll their volumes to future periods and carry their positions over to the next month, or they will need to flatten their positions and offset their exposure prior to the conclusion of the pipeline cycle.

Featured Articles

- Blog

The Price is Right - North America Crude Oil Price Differentials Explain and Foretell Market Shifts

There is no debate about it: The CME/NYMEX domestic sweet (DSW) crude oil futures prompt-month contract at Cushing, OK, is the most closely followed benchmark in U.S. energy markets. It’s the price quoted in nightly news reports and general media publications. And now, with U.S. exports of WTI deliverable on the Brent contract, domestic sweet at Cushing is arguably setting the price for crudes around the world. But the fact is, most crudes traded in physical markets across North America are not priced at the DSW-at-Cushing benchmark but instead at a differential to Cushing — higher or lower on any given day based on each crude’s unique quality, location, and supply/demand characteristics. In today’s RBN blog, we discuss how the behavior of differentials from the Cushing benchmark can go a long way to explain what is happening with crude oil production, transportation volumes, storage and, of course, exports.

- Blog

Future(s) Games, Part 2 - The Baffling Impact of Oil Futures on Physical Contract Prices - CMA Roll Adjust and P-Plus

On April 20, that fateful day in crude oil markets when the CME May contract for WTI at Cushing collapsed to negative $37.63/bbl, the number of contracts involved in the chaos was relatively small. So you might think that most producers sat on the sidelines, watching Wall Street paper traders writhe in stunning financial pain. But not so. Almost all producers saw their crude prices that day crashing in exactly the same magnitude. That’s because the daily price of the CME WTI contract is part of the formula pricing used in a very large portion of crude oil contracts in U.S. markets, both directly and indirectly. There are two formula mechanisms that are commonly used in crude oil sale/purchase contracts that are responsible for that linkage: the CMA and WTI P-Plus. These arcane pricing mechanisms are complicated, but in order to understand U.S. crude markets, it is critically important to appreciate how they work. Today, we continue our deep dive into crude oil contract pricing mechanisms.

- Blog

Trading in the USA - When Price Does Not Matter: Exchange Trading, Differentials, and the Cash Roll

As crude oil exports have become an integral part of US/Canadian trading, the market has evolved to accommodate this profound transformation. But the mechanisms used to price many of the most significant export grades are obscure and little understood outside a small cadre of professional traders and marketers. This is particularly true for the most liquid grades that employ a trading approach known as “exchange trading” or “spread trading,” in which volumes at regional hubs are valued in buy-sell transactions against domestic sweet crude at Cushing. In this context, “exchange trading” does not mean trading on a regulated exchange. Instead, it means trading via an exchange of barrels between buyer and seller. In today's RBN blog, we delve into some of the most complex aspects of this trading mechanism.