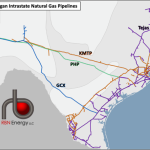

Kinder Morgan will expand its Gulf Coast Express (GCX) natural gas pipeline by 570 MMcf/d to move about 2.57 Bcf/d to the Agua Dulce hub in South Texas from the Permian Basin. The company announced on October 16 that it made a final investment decision (FID) to move ahead on a $455 million expansion of the 500-mile pipeline (blue line in map below) expected to be in service by mid-2026.

Featured Articles

- Blog

Help On The Way - Midstreamers Rush to Avert Permian Gas Takeaway Constraints

The U.S. midstream sector is clamoring to build takeaway pipelines for ballooning natural gas production volumes in the Permian Basin and get ahead of any developing takeaway capacity constraints. In the past year, a number of companies have floated plans for moving Permian gas supply east to the Gulf Coast, spurred on by two primary factors — expectations for accelerated supply growth in West Texas; and on the other end, emerging demand from a combination of LNG export facilities being developed on the Texas and Louisiana coasts, and the slew of export pipeline projects targeting growing industrial and gas-fired power generation demand in Mexico. These expansion projects are in a bit of a horse race, not just to beat the clock on potential transportation constraints, but also competing against an increasingly larger field to secure shipper commitments and make it to completion. Among the factors affecting their progress will be their in-service dates and their destination markets. Today, we provide an update on these competing pipeline projects, including the newest entrant, Tellurian’s Permian Global Access Pipeline.

- Blog

Blame It on Texas - Pipeline Alternatives Gunning to Provide Permian Relief

Natural gas supply growth from the Permian Basin has flooded the Texas market in recent months, filling up takeaway pipelines and sending Waha spot prices to steep discounts relative to its downstream markets. Incremental demand — from exports to Mexico for gas-fired power generation as well as for power demand in Texas — has provided some relief for West Texas prices in recent weeks. But Texas power demand is seasonal and, while Waha’s exports to Mexico are expected to continue growing, it’s likely to be on a piecemeal basis. Thus, longer term, new Permian takeaway capacity will be needed to balance the Waha market. To that end, there are a bevy of takeaway projects vying to expand capacity from the Permian. These projects — their timing and routes — will drive the Texas gas flows and pricing relationships over the next several years. Today, we continue our series on Permian gas, this time delving into the various takeaway capacity projects competing to move Permian supply to market.

- Blog

Turn the World Around - Perryville Hub's Pivotal Role in Transforming U.S. Natural Gas Flows, Part 2

Demand for U.S. natural gas exports via Texas is set to increase by close to 6 Bcf/d over the next few years. At the same time, Texas production has declined more than 3.0 Bcf/d (16%) to less than 17 Bcf/d in the first half of November from a peak of over 20 Bcf/d in December 2014, and any upside from current levels is likely to be far outpaced by that export demand growth. Much of the supply for export demand from Texas will need to come from outside the state, the most likely source being the only still-growing supply regions—the Marcellus/Utica shales in the U.S. Northeast. Perryville Hub in northeastern Louisiana will be a key waystation for southbound flows from the Marcellus/Utica to target these export markets along the Louisiana and Texas Gulf Coast, particularly given the hub’s connectivity and prime location. Today, we look at the pipeline expansion projects into Perryville that will make this flow reversal possible.